Portfolio Construction Part 2

Portfolio Construction Part 2

Match your portfolio to yourself

Disclaimer: I’m not an investment professional nor have any financial training. I write this substack for my own learning and pleasure. Stop here if you value your time.

I started this substack for personal reasons. I am not looking to seek an audience. I am not hoping that it will become an avenue for a side gig. I started this substack to help my investment process. Its primary purpose is to write down my thoughts so that I could revisit them and seek self-improvement over time. Although having feedback would be nice, I’m happy to share my random opinions with interested others. The reason I begin with this, is because it is important to understand my context in framing this next post.

As my disclaimer states, I come from a non-finance non-business background. I have no family members in business growing up. What I’ve learned only occurred after obtaining a science degree with some extra research training. Subsequent to finding a steady job, I recognized that I needed to figure out what to do with my savings. A mentor suggested reading the Wealthy Barber by David Chilton. I should have read this as a teenager but having no money and parents to provide from me, there was no desire. I can’t remember exactly how but I came upon the Intelligent Investor by Benjamin Graham fairly soon after. It was extremely boring with out-of-date examples but somehow, the spirit of finding undervalued companies resonated with me. The “how” was the difficult part. I signed up for the Value Investing seminar at the University of Western Ontario taught by Dr. George Athanassakos. It was a “how to” primer, exactly what I was looking for. Now I had the tools to be a successful retail investor, how hard could it be? This was the beginning of the rabbit hole.

It has been just over a decade since I dug myself into this hole. Have I been successful? Not really. Have I been lucky a few times? Absolutely. Was it worth it? I’ve learned a few useful things. Would I recommend it to others? Only if you are willing to do the work. What insights I have gained? This is the topic of this post.

“The most important thing is …..” - Howard Marks (Oaktree Capital)

It seems that the retail investor is forever beholden to the market mechanisms beyond our control. We get to pick up the scraps that sophisticated players leave behind. Retail investors are what is called Outside Passive Minority Interests (OPMI). We have no voice. We are subject to the whims of management. We don’t have privileged access to information. We don’t have the analytical horsepower to understand the nuances. It seems the game is really stacked against us.

This being said, learning and comprehending markets and businesses is still important. We still have to make decisions about how to manage our savings regardless of our skillset. A working knowledge of basic principles is key to financial independence, even if we don’t want to do it by ourselves. The probability of reaching this goal by sticking it in a savings account or randomly following friends into “advisors” aka salespeople, is not very promising especially in 2021. You could get into real estate because that is a sure win as conventional wisdom goes. But the promise of good certain returns can not be without work or aggravation. If you think you are getting a free lunch, you probably are the lunch.

The most important thing is know your self. This is an excerpt from one of reputable Wall Street Journal columnist.

Jason Zweig: Temperament Is Everything for Most Investors | Morningstar

I think temperament is incredibly important. The great investment consultant Charley Ellis gave a remarkable speech in Toronto many years ago, where he talked about the three ways an investor can achieve superior performance. And if I remember right, the first was what he called physical excellence, which basically means outworking everybody else. I mean, you can just try harder. And if you have superpowers, you can get up at 4 in the morning and work until 10 or 11 at night, reading annual reports and financial statements and doing all kinds of other fundamental research maybe you can just outwork everybody else. There aren't a lot of examples of people who've done that, but I'm sure there are some.

The other was intellectual superiority, where you're just smarter than almost everybody else. And there is lots of examples of people like that. But what Charley Ellis said in his speech was—and, of course, this wasn't completely accurate in his case, but it certainly is in mine--he said, since I can't outwork everybody else, and I'm not all that smart, I choose the third way, which is the emotionally difficult way. And I think he really put his finger on something, which is that having the right temperament is pretty much everything for--I don't know if it's 99% of investors, maybe it's 95%, maybe it's 90%, although I imagine it's higher--probably at least 95% of all investors. For most of us--the vast majority of us--intellectual superiority is out of reach, physical superiority isn't feasible. So, the one choice we have left is trying to be emotionally superior investors. And that just boils down to a handful of things. It means you exhibit self-control and you avoid self-delusion. You don't lie to yourself, and you play your own game instead of trying to play somebody else's game. And it sounds so easy, but it is incredibly difficult. And really to cultivate that kind of self-control and self-discipline, and lack of self-delusion is the work of a lifetime. And you can backslide and go down the slippery slope toward chasing the next hot dot in the wink of an eye.

And, as Richard Feynman, the physicist, said, “The easiest thing you can do is to fool yourself because you were the easiest person to fool.” And that's vitally important for everybody to remember. And you can't be vigilant some of the time, you have to be vigilant all the time, or at least you have to try.

So, temperament is, for most investors, everything, but it's the thing nobody wants to work on, because it's hard work, it's hard to measure progress. And most of the time, it's unrewarding and unsatisfying, because self-discipline mainly involves watching other people party and saying, I'm not going to participate.

I’m not the smartest or shrewdest person. I work hard but I’ve got a day job and family that I’m committed to. I don’t have a special knowledge network to tap into for unique insights. So the only advantage I can hone is an emotional one.

My trial-by-fire DIY investing over the past decade has taught me more about myself than anything else. I suffer a lot from my fear and anxiety of loss. I have patterns of behaviour that frequently recur as a result of my loss aversion when faced with common investing problems. Problems such as:

a) The stock I like is running up higher after I just finished study it. I’m afraid I’m going to miss out owning it if I don’t buy it now.

b) The stock I bought just tanked 50% in price. I can’t bear to crystallize my loss now. I’ll just hold on until I break-even.

c) My friends are making big bucks trading options and buying growth tech. My portfolio is doing nothing. Maybe I need to play their game too?

d) The stock I own just gained 100% after a year. I better lock-in my gains before I lose them.

I assert that focusing on these 4 items is counter-productive to long-term wealth creation and will reduce one’s quality of life. The more productive questions are:

What is my end goal to achieve financial independence?

How much time/work am I willing to put into thinking/learning about investing to achieve this goal?

What unique set of tools/skills/people do I possess or can develop in the future to better control my fears and create wealth over time?

Financial Independence

There are numerous calculators online to help ballpark what you might end up with at retirement. The key factors are 1) how much do you make after tax? 2) how much can you save? 3) what is your investment return? 4) how much inflation is there? 5) how much longer until retirement?

Assuming that the median Canadian annual salary for 30 -45 year old is ~ $50,000, after tax being $40,000. To get to ~ $1 million at the age of 65, you would need to save 30% of $40,000 = $12,000 per year, earn a 7.5% investment return against a 3% inflation rate (4.5% real return), and work for 35 years.

In 2021, is this reasonable? Although these are long-term averages, I fear these averages may actually misrepresent the future. The S&P 500 is at valued at historic highs, Canadian high-interest saving accounts are only yielding 1.25% annually, global central banks are continually putting money into circulation driving up asset prices, and with inflation spiking and it may or may not be transitory in the future. The expectation of achieving real investment return rates of 4.5% could be unrealistic. So, either one will have to earn much more, saving a lot more, or work much longer.

Using the same numbers, if one were to invest in the S&P 500 at these record highs, the investment returns may turn out to be 2%, inflation could increases to 4% with a real return rate of -2%. After 35 years of no after-tax income raises and a steady 30% savings rate, the total savings will be a paltry $300,000. The outlook is much more dismal if one’s working life is shorter or if the savings rate is much lower.

With these ideas in mind, it is not surprising that people are chasing high growth returns with cryptocurrencies, non-fungible tokens, and the promises of next generation ideas like the metaverse. And because the passive indices representing the stock markets has done so well in the recent past, there is a rush to DIY investing with low cost exchange-traded-funds (ETFs).

The one thing I’ve learned over the past decade is that it is important to not be dismissive of new ideas and their future potential. Ardent value investors unwilling to open up their imaginations or adapt is not the right approach either. The key is to figure out how much risk I’m incurring relative to the expected return I could receive in the future. I’ve bought some Bitcoin to learn about this space. The most important thing is how much time I willing to spend learning and thinking about investing for my retirement.

Time well (not) spent?

There is an old Japanese concept called the Ikigai. This is best depicted in the picture below:

The reason I bring this up is that each one of us needs to evaluate how we use our time. We all have the common goal of working and saving for retirement. It is conceivable that you rather listen to fingernails scratching a chalkboard than studying the financial markets, learning how to do valuation, and managing your own finances in your spare time. I do it because I enjoy the challenge and the joy of the eureka moment when I figure something out. But I’m a bit nuts.

So for the average person, even if you rather do something else or if you want to learn but have no existing tacit knowledge, what is the best way to start investing?

I’ll first begin to tell you want NOT to do because I’ve done it and it was pretty stupid. Don’t:

read a couple of books or take a course and think it’s easy to do on your own.

take a lot of your savings and put a large % of it into an individual idea after a novice attempt at analysis (aka look at the stock chart, read a few headlines, be overconfident in your spreadsheet forecasts, be over-trusting of social groups to provide good advice, etc).

do nothing and put into a savings account.

trust salespeople without doing your homework (eg whole life insurance).

If I could go back in time, I’d use the following concepts:

Use the 1/N rule to construct a portfolio of non-correlated asset classes. As the myth goes, the famous inventor of the modern portfolio theory, Harry Markowitz, who won a Nobel prize for his formula, when he retired didn’t use his own formula to manage his savings. He instead used the 1/N rule. For most us, this would mean equal allocations of 25% cash/bonds, 25% gold, 25% equity, and 25% real estate. I would use a series of low-cost ETFs to express this view. For those interested in a detailed research paper on 1/N vs optimal portfolio performance, click on this link.

Find a way to automate it to minimize any bad behaviours (trading in and out of stuff) in addition to forced rebalancing at regular intervals (quarterly, biannually, or annually). As of today, I like Wealthsimple’s automated platform but would prefer to have more control to express the 1/N rule. So I would need to find a discount broker, create a tracking spreadsheet and generate automated reminders to rebalance the portfolio over time. Alternatively, find a wealth manager and pay them for advice +/- let them manage it for you.

If desired, take a small % of my savings (<10%) to pick individual stocks/bonds to put some skin in the game. The goal would be either to learn or just have some fun gambling. What separates the 2 is very thin, so be very clear in your intent and be careful becoming too overconfident about the outcome. The former is about developing good processes whereas the latter is focused on the final result of the bet.

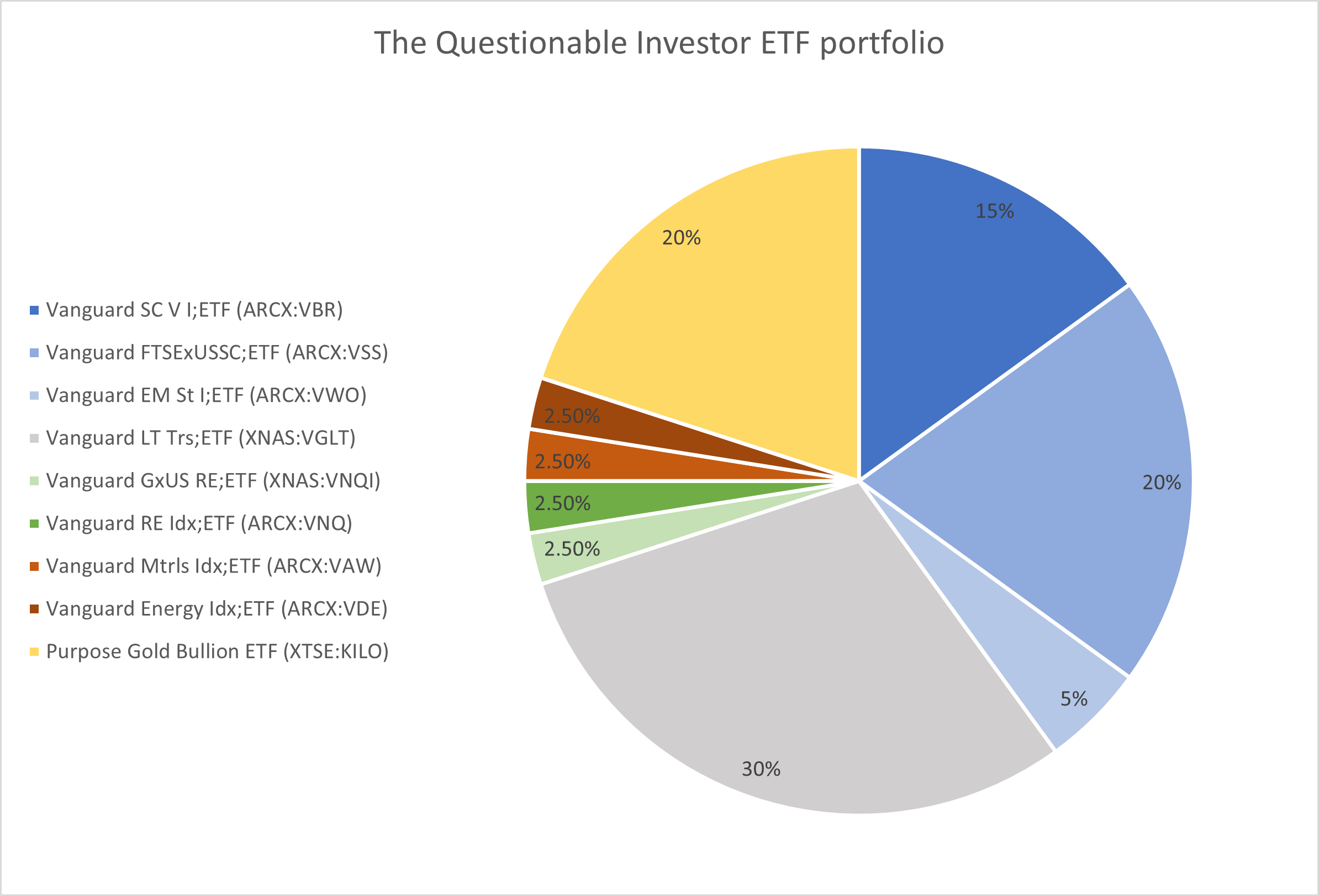

Earlier this year, I came across a website called Portfolio Charts from a twitter account I follow: @ValueStockGeek. The website allows me to use historical data to retrospectively tinker with an ETF portfolio and see it’s return, maximum drawdown, duration of down years, and how much I could pull out of it after retirement without eroding the principal. I started off with the 1/N rule and modified it to produce the best outcome.

This ETF portfolio has 40% in equity tilted towards small cap and value. It has 30% in long-term US treasuries. It has 5% in real estate (equally weight between global and US). It has 5% in materials and energy. And finally, it has 20% in gold. The gold ETF I’ve listed is new, but it allows you to redeem for gold bullion if so desired. The annualized return would be 7.6% with a maximum drawdown of 17% lasting at most 3.5 years. The perpetual withdrawl rate after retirement is 5.8%. It has an ulcer index of 3.3. The expected management expense ratio (MER) is 0.114%. Alternatively, @ValueStockGeek developed his weird portfolio and his design rationale can be found here.

For those that have a higher risk tolerance and can withstand volatility (aka the big wave surfers out there), you could also approach this problem by using the Barbell strategy. This was popularized by Nassim Taleb in his book Antifragile. It combines extremely high-risk ideas with extremely low-risk ideas, avoiding everything in between. An example of this would be a portfolio that held 90% in cash and short-term fixed-income instruments (eg GICs) and 10% in very high-risk/high-uncertainty bets (eg cryptocurrencies, non-fungible tokens, out-of-the-money options on meme stocks, private venture capital funds). This would require you to invest in 20-100? high risk ideas and a bit of leg work. A low risk way to actualize this is to use the interest received from your GICs to fund these bets.

Needless to say, there are many ways to approach this “what to do with my savings” problem. The approach to take depends on the unique set of tools/people/skillset and temperament that you have now and what you can develop to serve you in the future.

It has to be your approach!

When deciding how to put together your own personalized approach to investing, it is important to do a little survey of your environment and yourself. Here is a sample of questions to ask yourself:

How much base financial knowledge do you really have? Who and where did you learn this from? Do you have continual access to unbiased people that can give you thoughtful advice? Does your relationship network give you opportunities to tap into a specialized skillset (eg your parents are commercial real estate agents)?

How much real-life experience do you really have investing your own money? Are you an anxious person? Do you have a tendency to worry and lose sleep over stressful events? What kind of support system do you have at home? Does your partner have a similar disposition?

How do you deal with uncertainty? How willing are you to venture out of your comfort zone? Do you have a growth vs fixed mindset?

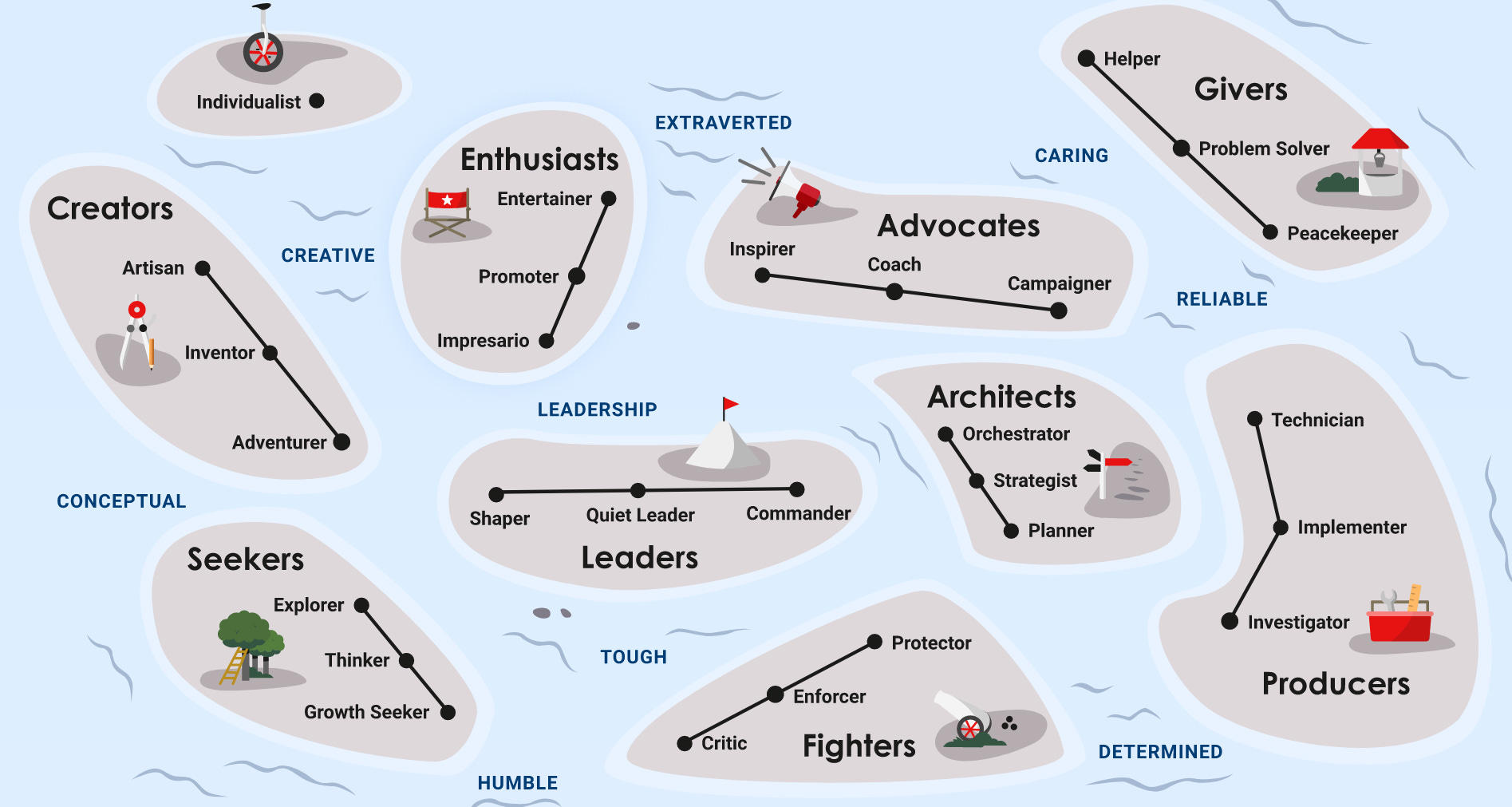

Although I’m skeptical of the predictive utility of personality tests, I think they have some ability to give insight into an investing approach that resonates with you. My 2 favourite ones are the Big 5 Personality test and Ray Dalio’s Principles You test. The “Big 5 Personality” test is a popular measure of openness, conscientiousness, extraversion, agreeableness, and neuroticism. The Principles You test gives a more detailed breakdown of 28 archetypes as seen below:

A distress/deep value investor needs to score high on conscientiousness, low on the agreeableness, and be highly individualistic in order to be successful. A venture capital or angel investor needs to scores high on openness and extraversion, and have a growth seeker archetype to be successful. A highly agreeable and neurotic person would be more successful adhering to an automated portfolio allocation method to avoid FOMO (fear of missing out) and failure to crystallize certain losses when a stock moves the wrong way for the right reasons.

Gavin Baker published a cliff notes summary of the book “The Art of Execution” by Lee Freeman-Shor. The book describes 5 tribes:

Rabbits = do nothing when losing money

Assassins = quick to take losses

Hunters = averaged down when losing money (with the caveat of limiting the absolute maximum loss, not averaging down on highly indebted businesses, and business that face obsolescence)

Raiders = quick to take gains and sell their winners

Connoisseurs = slow to sell their winners

The most successful investors are Assassins/Hunters when losing and Connoisseurs when winning. The most important thing is to have a robust process that helps you make, on average, better decisions over the long-term. By having insight into your particular situation, play on the advantages you have, and reduce the risks of making unforced idiosyncratic behavioural errors. This is the key to sustainable wealth creation.

My investment process roadmap

Hindsight is always 20-20. I’m not sure that not making all these mistakes over the past decade would have gotten me to the same place I am today. But if I could start over, I think taking more time to craft a roadmap would have been helpful.

As I opined earlier, I would have put my funds into a series of ETFs using the 1/n rule. If I did it today as a novice, I would break up my portfolio into 3 strategies: a) the Questionable Investor ETF portfolio (45%), b) the barbell strategy using 1-year GIC interest to fund my cryptocurrency purchases (45%), and c) individual stock selection based on a checklist of criteria (10%). I would be diligent with keeping a journal to document my decisions. I would write a substack/blog to explain my ideas and thought processes to others. I would write down my guidelines explicitly.

My current portfolio is 8% cash and 92% stocks composed of 36 positions. I plan to introduce over time to include the Questionable Investor ETF portfolio and the barbell strategy. My investment process usually involves completing a business quality checklist to help me size my position. I use a variety of resources to do my research (regulated filings, podcasts, YouTube, research papers, etc). I try to both estimate what would be a reasonable range of values to achieve a decent rate of return, as well as the price-implied expectations for the business. I include basic technical analysis to find decent entry points (it would be arrogant to disregard techniques other market players use). I generate a quick and dirt valuation calculator based on the 3 - 5 big fundamental drivers for each of my positions to keep me grounded.

I know that when positions turn against me, I tend to be a rabbit. I know that I also gravitate to be a connoisseur with my winners. To capitalize on these behavioural tendencies, I try to buy higher quality businesses or unencumbered assets with asymmetric upside optionality that I can hold for long time periods (5-10 years). I start off with small purchases and average into a position over time, capping out at a maximum of 5% of my portfolio at cost. My goal is to buy well and hold for the long-term, allowing my winners to concentrate on their own. Ideas that are illiquid, small, and untested, demand more downside protection which in my case is smaller maximum position sizes or purchases at very low valuations. Finally, I try to write things down so that I can revisit them in the future unpolluted by narrative revisions from memory recall.

I tend to have lots of ideas, be too optimistic about the businesses’ futures, and lack patience in waiting for prices to come to my threshold. The processes described above helps keep me in check. It is still a struggle but slowly I think I’m headed in the right direction.

This is my process that fits my situation (a one-person gong show) but hopefully, this substack article will give people some colour how to think about their own portfolio design decisions.