My Meta Platform Bet

My Meta Platform Bet

Disclaimer: I’m not an investment professional nor have any financial training. I write this substack for my own learning and pleasure. Stop here if you value your time.

Since the beginning of 2022 just before the stellar market correction, my attention was piqued with Meta Platforms’ drop from $350/share to $230/share. It hit its 200 weekly moving average and I thought that things might start getting more interesting. I bought a few call options to put some skin in the game and force myself to dig deeper. So down the rabbit hole I went (along with the price action).

Meta Platforms’ history is well known to many. Books, traditional media articles, substacks, tweets, reddit posts, etc detail this company’s accomplishments as well as its trials and tribulations. Mark Zuckerberg (MZ) created this social media giant when he was 19 years old in his Harvard dorm room and scaled it to the world where 3.7 billion people out of 7 billion have at least one of their Family of Apps (FOA) – Facebook, Instagram, and WhatsApp. Its rapid scaling and success with connecting the world was initially lauded, but as it tried to maintain growth, it was careless with user data privacy, facilitated nation state population manipulation, and brought out all the messiness of human affairs. It also uncovered the path to which new social media companies can follow and follow they did. Now Meta Platforms faces competition from the likes of TikTok, SnapChat, BeReel, Telegram, Signal, and anything else that competes for people’s time. On top of this, our beloved Apple, in its benevolent way, for the good of its customers, rolled out the App Tracking Transparency (ATT) Policy, which requires customers to grant consent for mobile apps to track their activities. This prompt is worded in a way that biases clicking “no” for non-Apple apps and “yes” for Apple’s in-house apps. Shortly after rolling out ATT, Apple is now changing its App store 30% developer tax to encompass social media boosts, so that it can take a cut of the very lucrative advertising revenues that flow through many of its free apps. Where Steve Jobs was a mentor to Mark, Tim Cook despises him. Nothing personal, it’s just business. Finally, the icing on the cake, was MZ’s renaming of Facebook to Meta, and allocating $100 billion over the next 10 years to develop this nebulous “Metaverse”.

Ben Graham’s “The Intelligent Investor” describes 3 areas of opportunities for Enterprising investors, one of which is the relatively unpopular large company. He writes that large companies as opposed to small ones, have a double advantage of having the financial resources and human capital to carry them through temporary adversity as well as the market likely responding to improvements with reasonable speed with so many eyes on them. The key is temporary. How temporary is the impending ire of government oversight? How temporary is the intensity of competition for attention? How temporary is Apple’s monopoly power? How temporary is the massive investment in the Metaverse? Arguably, none of these elements are temporary but more likely secular. It is not surprising that the financial community and shareholders have removed $688 billion of market capitalization from the stock or a 70%+ decline from the peak.

There is a bit more nuance than meets the eye especially when digging deeper in the story. This coupled with such a massive price decline, could it be possible that Meta is undervalued and there are unappreciated assets worthy of an investment? Aggregating several concepts touted by great investors such as 2nd level thinking, competitive advantage period, capacity to suffer, ability to re-invest, portfolio concentration, and asymmetric outcomes provide a foundation to approach Meta.

Lollapalooza of secular changes and its impact on Meta and its ecosystem

Apple, government regulation, and low barriers to entry in the social media space are secular in nature. This 1-2 punch hits Meta from a profitability and growth standpoint. But 2 considerations less talked about include the rising cost of capital and the inherent nature of intangible-based businesses. I hypothesize that the combination of these factors will reduce the pace of venture capital to fund new social media businesses, it will be a forcing function for founders to achieve earlier profitability at the cost of limiting scale, failing social media start-ups will have low exit barriers, and incumbents can easily clone their “killer” features. I will warn readers that I have no special access to data and what I present is what I can scrape up from Google searches.

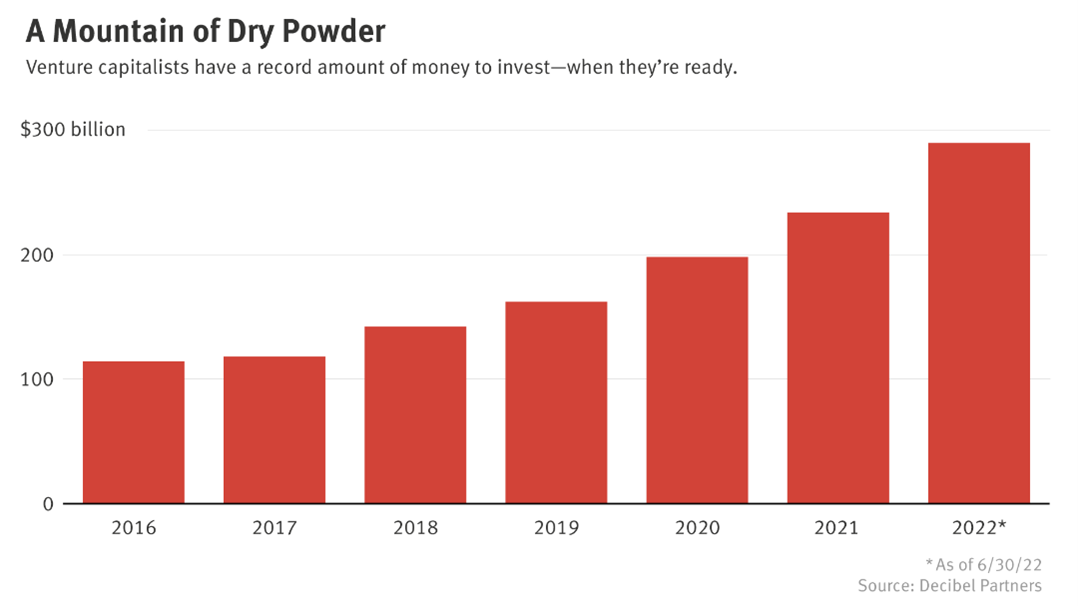

With rising interest rates and 20%+ pull back on the public markets, limited partners of venture capital funds are suffering from mark-to-market losses. Many are likely reassessing their % allocation to illiquid high-risk investments, finding safer, more liquid alternatives, and possibly asking their VC partners to slow the pace of capital deployment in new start-ups. VC partners are asking their founders to watch their cash burn, focus on measured growth and more likely to investing in portfolio companies than add new ones. New and existing founders raising capital may have accept lower valuations and the bar to get funding is going to be higher. That said, there is about $230 – 290 billion of dry powder still out there. Below are a few articles supporting this perspective.

https://www.ft.com/content/7cbae3f3-8197-4816-aba8-860cac76cbb4

https://www.ft.com/content/27475580-230f-4581-8b50-16f8aafe4a4e

https://finance.yahoo.com/news/venture-capital-is-seeing-a-slowdown-sidelines-133309996.html

This funding slow down coupled with Apple’s ATT policy, is a double whammy particularly for younger social media businesses. Using publicly available data, my best estimate is that Apple accounts for 17% of the smartphones in use today if the following facts are true: the average iPhone user retention rate is 82%, smartphone lifespan is 4.6 years with a cumulative 2.2B iPhone sold over the past 15 years, this equates to 1.15 billion iPhones out of 6.65 billion in use today. Furthermore, if Apple’s App Store successfully imposes their 30% tax on social media advertising revenues, this would equate to an additional $5.10 cost of revenue per $100 revenue received. If gross margins were 70% before this change, it would be 65% after this change. It’s ugly out there for social media businesses especially the ones at an earlier stage.

This is from Evan Spiegel, CEO of Snap, from their Q3 2022 conference call.

“what informs our strategy as we think about navigating this difficult macro environment that has impacted our advertising business over the past few quarters. So we made the decision to reprioritize and focus our investments on our 3 strategic priorities: growing our community and their engagement, reaccelerating and diversifying our revenue and investing in augmented reality. And these changes should allow us to drive continued growth in our community while delivering free cash flow even with low levels of revenue growth. And that gives us a lot more flexibility to focus on the long term in an environment where the cost of capital has increased quite dramatically.”

These headwinds combined with elevated customer acquisition costs compared to the pandemic lock-down period, Snap’s Sales & Marketing expense per incremental DAU has reverted to ~ mid $30 per DAU (similar to pre-pandemic) up from mid $20. With Snap having decent scale at 363 million DAU in Q3 2022, it will be even more challenging and costly for smaller social media start-ups to compete for people’s attention. It is my belief that this environment, on the balance of probabilities, will lead to slower growth and a higher failure rate for the social media ecosystem. The extension to this belief, is that incumbents, such as Meta, will relatively benefit from weakened competitors because they’ve already built up a user base that already comprises 60% of the global smartphone population (6.64B global smartphones of which 1.02B are in China, Russia, and Iran where FB is banned). With social media businesses opting to use cloud providers for their computing infrastructure, they have few barriers to shut down their businesses and fire their employees if user growth does not take off.

This leads to the concepts described in the book Capitalism without Capital by Haskel and Westlake. Here the authors write about the 4 characteristics of intangibles: scalability, sunkenness, spillover, and synergy. MZ has repeatedly demonstrated this ability to incorporate the ideas of others into his products, from his Harvard competitors to his original facebook concept, to Timehop’s ‘On This Day’, to SnapChat Stories (Instagram Stories), to Zoom and Houseparty (Messenger Rooms), and most recently TikTok short-form videos (Reels). With almost 10,000 social media startups listed on Crunchbase, there are plenty of features that when plugged into the FOA machine, bring more dollars to Meta than its smaller competitors given its established installed base. This ties back to Meta’s scalability and ability to enjoy the fruits of others via spillover effects. So, despite, headwinds on its profitability and growth, Meta’s competitive position has improved and arguably its competitive advantage period may have lengthened.

Being John Malkovich (or Mark Zuckerberg)

The financial community is up at arms with respect to MZ’s uncontrolled expenditures both in term of opex and capex. During the Q3 2022 conference call, I could hear the collective gasps from the analysts when Dave Wehner (CFO) guided that 2023’s opex is going to be higher, headcount will stay the same, Reality Labs’ operating losses will be greater, and capex will be 10-20% higher than 2022. It was shortly after this call, Meta’s stock price plummeted from $135 to $88/share. Twitter and all message boards lit up, is Zuckerberg on crack?!?!

Perhaps to answer this question, it is useful to read Steven Levy’s Facebook – The Inside Story. It details the backstory of Facebook’s rise and collected stories of MZ through this period. The truth of how MZ’s mind works according to the book is obviously fraught with high degrees of error and must be taken with a grain of salt. That said, the following observations of his 20-year-old self may be useful (thought processes are often well formed by this time and likely becoming ingrained decision-making habits by age 25 according to Sandra Aamodt, neuroscientist and co-author of the book Welcome to Your Child's Brain):

- He is capable to learning from mistakes and often does his learning in public by pushing out products then iterating on them (Facemash, Synapse, CourseMatch, ZuckNet, Art History group study program)

- He is strong willed but adaptable as demonstrated by his pivot away from Wirehog once data became apparent to him that it would not be scalable due to the intensive opposition by the Record labels.

- He is focused on work first and enjoyment later such as when his young startup team started goofing off, he would encourage/force people to finish their work before going to the movies.

- He demonstrates courage to act in a counter-intuitive manner such as rolling out Facebook to Columbia university after Harvard because he wanted to see how his product measured up to an existing competitor.

- He focuses on building things that he would like to build for himself, not what a market map identifies as a need and trying to fill that gap.

- Even during the Myspace days, MZ viewed FB is a technology company whereas MySpace saw itself as a media business.

- When faced with the pragmatism of advancing FB the business versus honoring a handshake, he chose the pragmatic route (Don Graham’s deal).

- Persistent willingness to sacrifice short term gains, such as the possibility of NewFeeds reducing profile clicking and thus what initially thought would reduce ad exposures as well as his, more recent, discussions about prioritizing engagement with Reels despite cannibalizing existing well-established monetization features.

- In the early days, MZ viewed user objections are transitory, data primacy over narrative was their initial modus operandi, but learned the hard way, that this is not sufficient. This is illustrated by their formation of their Facebook Oversight Committee to deal with complex content moderation issues.

https://www.oversightboard.com/

- MZ once said to Dave Morin – “Apple is an innovation company, FB is a revolution company”.

- Dave Fetterman’s idea of opening up their network to allow 2-way permissionless user data transfer between tech companies (eg Amazon and FB) was broadly opposed by FB’s brain trust, but only MZ was open to the idea of opening up their closed network system.

- Move fast by pushing out code 3-4 times a day versus weeks to years violating conventional software development dogma at the time.

These subjective examples illustrate MZ’s willingness to be unorthodox and move with urgency, frequently sacrifices the short-term gain for long-term growth, and he is more interested in product potential and possibilities than just optimizing for maximum profitability. With every performance ad-supported attention-based tech business pulling back investment and reducing headcount to shore-up their balance sheets in the face of various headwinds, Meta’s strategy seems very unconventional. If MZ is still the MZ as depicted in these stories, this might begin to make a bit more sense.

A large part of Meta’s $35+ billion capex spend is to build out their AI infrastructure (AI Research Supercluster [RSC]). For example, they’ve purchased 760 Nvidia DGX A100 systems where each cost ~ $170K. Once complete, Meta will own and operate one of the world’s largest AI super-computer. This gives them ML superpowers for their existing social media properties, to drive recommendations, provide more accurate probabilistic-based attribution ad-models, and give them algorithm-based content moderation capabilities, as well as their metaverse initiatives. Meta is taking a page out of Amazon’s playbook; build out your own tangible physical assets with urgency (18 months in their case), have the freedom to operate independently, and couple this with existing intangible assets, to reduce their fragility. With billions of messages and videos crossing their platforms daily, moving fast and feeding their ML algorithms before others have the chance to develop theirs, will lengthen their competitive advantage period.

https://spectrum.ieee.org/meta-ai-supercomputer

https://www.theverge.com/2022/1/24/22898651/meta-artificial-intelligence-ai-supercomputer-rsc-2022

Furthermore, with recent geopolitical tensions between China and the US culminating into the recent US-based semi-conductor EDA software ban. It is not inconceivable that further supply chain disruptions can occur since most of the world’s current semiconductor manufacturing capacity (TSMC and Samsung) is geographically close to China. It is also not inconceivable that future costs for such equipment will be even higher especially with near-shoring efforts of fabricating capacity back to the US. In my opinion, Meta moving fast and building out their AI infrastructure now seems to be a smart decision.

Absolutely, this is all speculative trying to empathize why MZ has constructed his strategy the way it is. Certainly, their track record of traditional capital allocation is sketchy given that the majority of their public stock buybacks occurred at peak prices to offset the extremely generous stock options offered to their workforce over the years. MZ is a product engineer at heart, not a financial engineer. With many tech company stock valuations cratering (except Apple), many will need to revisit their future compensation philosophy. The egregious Silicon Valley practices of the past will need to be questioned if they don’t wish to eviscerate their employee morale. The saving grace is MZ’s total net worth is tied up in his company accounting for 13% of the ownership, and with him committing 99% of his worth to the Chan-Zuckerberg initiative, I am fair certain that even MZ will want Meta’s market cap to grow over time. It will be important to carefully to watch, Susan Li, the incoming CFO and her attitude towards capital allocation. She has been with the company since 2008. Her background came from finance and from the one fireside chat I found on the internet, she certainly is touts a return on assets framework.

I will have to see how she thinks of all this from an intrinsic value framework. Hopefully, they are open to the some of the ideas coming from the financial community. If MZ is smart, incorporating some of this into his mindset, will give him greater staying power to fund his Metaverse pivot.

The Venn diagram of Capacity to Suffer and Sizing an Innovation Bet

On the surface, the Metaverse bet, is a massive investment with an unclear outcome. According to MZ, it might cost $100 – 150 billion over 10 years, with most of it through their income statement. Undoubtedly it will also require capex spend, but this additional capacity is more flexible and could be used for its FoA as well. The PV10 of this bet is ~$25 – 38/share (if you trust MZ’s will stick to his own guidance).

He is building the rails for this reality and history would tell us that those who move first might not reap the final benefits. Bell Labs (personal computing), AT&T (internet connectivity), and railway operators (rails) are just a few examples that even if getting the vision right but being too early may not translate into a profitable business. Others have criticized that Meta has never innovated any hardware (FB phone, FB portal) successfully in-house and their primary success come from external acquisitions (WhatsApp and Instagram). Others are laying down bets that if virtual and augmented reality technology is to take off, Apple will be the primary benefactor, given their hardware innovation expertise and already sticky software ecosystem. The financial community would much prefer if MZ move slower with much smaller amounts. Parallels are made between Google’s (other bets) and Amazon’s (Alexa) approach to innovation. I’m not an Amazon expert, but it is commonly told that Bezo made several unsuccessful venture capital and wild bets with Amazon’s capital, but he never put the company at risk. For example, the development of Alexa, cost it 2.1% and 2.6% of their 2016 and 2017 R&D budget respectively. Put another way, it cost them 0.68% and 0.9% of their gross profits those same years. In contrast, Meta’s Reality Lab spend, is much higher when viewed in the same manner.

2021 Gross profit $95B, $12B Reality Lab expense on $25B of R&D cost (48% of R&D, 13% of Gross Profit)

2020 Gross profit $69B, $7.8B Reality lab expense on $18B of R&D cost (43% of R&D, 11% of Gross Profit)

2019 Gross profit $58B, $5B Reality lab expense on $14B of R&D cost (35% of R&D, 8.6% of Gross Profit)

In the value investing circles, there is a conventional wisdom that superinvestors often concentrate their bets, making a single position > 10% and sometimes up to 30 – 50% of their portfolio. Obviously, this is not always the case, as some have done very well with highly diversified portfolios with up to 100 positions. I wrote an article earlier about position sizing based on Zeckhauser’s framework. As a reminder, he discusses concepts such as complementary skills, the advantage multiple, and investing in uncertainty vs ignorant outcomes and to paraphrase his conclusion: If you possess a unique complementary skill that surfaces a significantly larger return than others OR there is no competition due to the fear of the unknown and unknowable future outcomes (which is reflected in bargain pricing), the greater the amount of capital you can put into the bet.

From this perspective, how does this apply to MZ’s Metaverse bet? Well, the metaverse is a pretty niche idea with popular media laughing at MZ’s explanation of it (imo MZ is not a very good salesman). The fact that people can only see gaming and maybe virtual corporate meetings as the endgame, how big can the total addressable market be? I would say at this juncture, no one knows with any degree of accuracy. Furthermore, the level of innovation and capital commitment to develop such a reality, is going to be enormous. Asides from the marketing-bent whitepaper by McKinsey on the metaverse opportunity ($5 trillion by 2030!!), the infrastructure needs to improve to the point where network and processing power is sufficiently quick to manage the data without any lag and the human-computer interfaces need to be mobile, unintrusive, and affordable all at the same time. This and convincing enough people to don these new interfaces to interact with each other. For any business leader, it seems asinine to pour large amounts of capital into this.

The internet was born out of DARPA, a government research division. It’s hard to figure out the development costs to get the internet to where it is today but some say that US government spent at least $1 billion (inflation adjusted dollars - $124.5 million) to seed the development of ARPANET that turned on after 2 years of R&D in 1969. We enjoy this end-product from collaborations between public and private efforts through a combination of open source and proprietary contributions. Certainly, the cost to develop the internet is very likely much higher than this number. With a 92% penetration rate, in 2020, the US internet contributing ~ $2.45 trillion USD to its $21 trillion GDP. My guess is that the internet (ex-US), contributed $6 trillion USD to an ex-US GDP of $74 trillion in the context of 65% penetration rate. A conservative estimate is that the internet’s TAM is at least $8 trillion today. If the metaverse is 5 – 20% of this value, we are potentially looking at $400 billion to $1.6 trillion in revenues. Is there a potential that is number is understated? I don’t know but it is possible.

Google spent ~$895 million on their Google glasses. Although it was a consumer failure, it does have niche applications in industry with suggested productivity gains in manufacturing, logistics and even healthcare. Microsoft, up until 2022, was working on the HoloLens, which was born out of their Xbox Kinect team. It, too, was a failure, unable to create adoption despite interesting potential applications. Apple has been very secretive about its VR and AR activities, but quietly developing patents over this period. With these capital-rich tech titans, all failing to move successfully to the next human-computer interface paradigm, what gives Meta the chutzpah to succeed where everyone has failed so far?

https://www.engineering.com/story/how-is-google-glass-doing-in-enterprise-and-industrial-settings

https://www.google.com/glass/start/

https://www.webfx.com/blog/web-design/the-history-of-the-internet-in-a-nutshell/

https://sites.cs.ucsb.edu/~almeroth/classes/F04.176A/homework1_good_papers/Alaa-Gharbawi.html

https://www.nytimes.com/2012/09/23/magazine/the-internet-we-built-that.html

https://www.wired.com/story/microsoft-hololens-2-headset/

What is MZ’s special sauce (aka unique complementary skill)? Of course, all of this is speculation, but in my opinion, it boils down to 3 factors:

a) Their “existential” threat as a powerful motivating factor. The recent moves of Apple and their 98% reliance on a cyclical digital advertising industry makes them very vulnerable to shifts that are out of their control. The playbook of social media is now well-known, and low barriers of entry will constantly challenge their media properties. They have also gotten to the size where unfavorable regulatory oversight and populist media can assail the trustworthiness of their products. Google, Apple, and Amazon do not necessarily face these threats. Perhaps Apple is the best positioned given their products are the physical access point to the internet and they have full control of their operating system. In tech, where scaling up is explosive but maintaining it is vastly harder relative to non-tech businesses. MZ has always worried about this sword of Damocles dangling over Meta’s head and understood the need to free from this threat. Even in Facebook’s early years, he perceived the necessity own their own operating system and hardware.

b) An understanding that large-scale human communication paradigm shifts, such as this, require open partnerships to better position for success. Facebook was the first global communication tool. The ability to connect humans is a messy affair. Their original ethos of move fast and break things seem correct at face value because it’s just people sharing messages and photos of their friends and family. How much harm could there be? Nothing here is mission critical. But as we have learned, communication at scale, with internet permanence, and the virality of social networks, breaking things at scale is a reality and can be extremely harmful. It would be prohibitively expensive (and harmful to those) to moderate content by hand and at the same time inadequate for one person or one company to be the arbiter of the “truth”. If nothing else, it would be very hard to imagine that MZ learned nothing over the years from all the scandals that have plagued their FoA. With their ML algorithms, establishment of the Oversight Board, and the build-out of their AI infrastructure, coupled with their willingness to partner/collaborate with industry players big and small, to create a safer global social network with the goal to develop scale economies shared, in my opinion, is the better strategy moving forward. Apple could build an impressive VR and AR product, but their philosophy of one vertical stack with a closed ecosystem, gives them fewer incentives to take on this herculean task with vigor, inspire others to build with them, and take on such moral responsibility.

c) MZ’s focus on the long-term product vision, unique decision-making habits, and unchallengeable control of Meta’s direction are necessary to do this in public scrutiny. Among the FANGMA (Facebook, Amazon, Netflix, Google, Microsoft, and Apple) companies, only “Facebook” and Netflix continue to be founder-run. Reed Hastings is 62 years old. It is very likely that MZ will be only founder left standing in the next 10 years. At the age of 38 years old with controlling class A voting shares, only Meta, can truly focus on long-term value creation and ignore the short-term market sentiment. However, this also removes any ability for external activists to agitation for financial shareholder returns if things take a turn for the worse or MZ becomes completely irrational in the pursuit of actualizing the metaverse. Despite, the fact, that Meta has excessively given out stock options and bought back expensive shares to prevent numeric dilution causing value destruction, MZ does have redeeming capital allocation qualities. MZ has demonstrated repeated willingness to cannibalize his products, tolerate short-term financial pain, and focus on user engagement metrics. He is willing to experiment (Libra, NFTs, Oculus). He can often understand product value before others (WhatsApp and Instagram). He has demonstrated focus and urgency to act when faced with threats (Facebook’s move to mobile). He is also capable of shutting down product ideas when the data is overwhelming negative (Facebook phone, Portal, Libra). Without knowing him personally, MZ appears to be a learning machine, proven to execute, and shown the ability to be adaptable.

With this special sauce, how would this look like in the future? My guess is as good as anybody else’s, so here is how I approached it. If the present value of the investment is ~ $68 to 102 B, I would think that at minimum with this degree of effort, MZ would expect a 10x return ($680B to $1T). Assuming a market multiple of 15, this would equate to $45B to $68B in earnings. With a tax rate of 25% and a pre-tax operating margin of 30%, he is expected a future top line revenue of $200B to 300B (PV10 $77 - $115B). This would mean that MZ is hoping that his company will dominate 7 - 20% of the internet’s estimated metaverse revenues. That’s a big hairy audacious goal.

Judging probabilities is difficult. Kahneman would say that people are reasonable at the extremes, but their behaviors are not. So, if the chance of success is 5%, the expected reward is ~ $3.60 - $5.25/share after netting out its investment capital; if the chance of a big fat zero is 95%, the expected loss, is - $24 – 36/share. Using the midpoint of these estimates, the net expected outcome is - $25/share. Will it be a zero? Go check out their real-time language translator and their pass-through capabilities on the Quest 2 Pro. Decide for yourself.

So, how much of the company is MZ betting on the metaverse? If you believe the market is correct in valuing Meta at $90/share, then he is wagering ~28% of the company. If, instead I use my intrinsic value estimates, it would be more like 14-17% of the company. Regardless, it is a concentrated bet, but not much different than some of the superinvestors of Graham and Doddsville, and here MZ is not an outside passive investor. That said, to hold Meta means being wed to MZ’s vision for better or for worse. If you think this metaverse is an absolute dead end, best to not get married to it at all.

Even Barry Diller would like to own the Blue App

Historically speaking, businesses in terminal decline face one of two choices, manage for liquidation by return capital to shareholders with dividends and opportunistic buybacks or make a Hail Mary bet, often in an unrelated or marginal adjacent field. The former could create shareholder value and the latter, often, destroys value. The common narrative is that FoA is in terminal decline and MZ is making a Hail Mary bet on the metaverse.

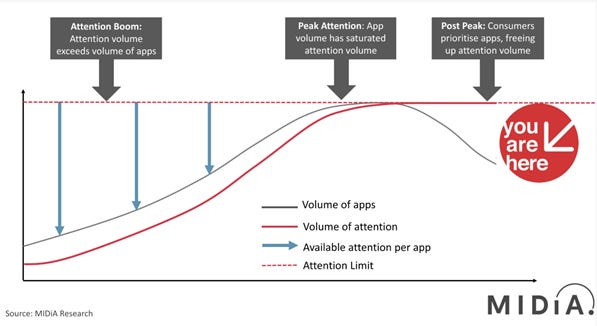

The major limiting factor of social media is the total amount of attention it can capture. This is a function of total time spend x total number of people.

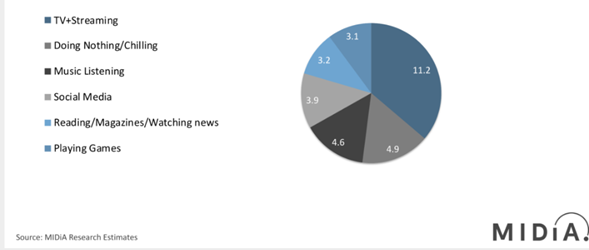

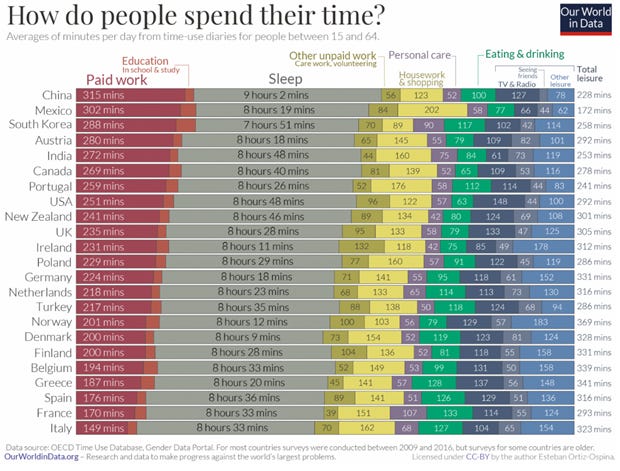

The 2nd graphic shows the # of hours per week people spend doing various things, which translates to ~ 4.4 hours per day. Using just Canadian data (https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=4510001401), people spend ~ 0.9 hours socializing, 2.1 hours watching videos or TV, 0.4 hours reading or listening to music, people spend 0.5 hours shopping, 1.1 hours of active leisure, and 3 hours of unpaid work. A great webpage of world data on time spent can be found here (https://ourworldindata.org/time-use). This suggests among OECD countries, we spend on average 118 minutes (3.5 hours) watching TV or listening to radio, 94 minutes (1.6 hours) with other leisure and 52 minutes (0.9 hours) seeing friends. In 2022, according to Oberlo, people spent 147 minutes (2.45 hours) on social media globally. That’s 41% of our free time.

With Meta already having 3.7 billion people on one of their FoA, and it hard to imagine that they can achieve more growth from acquiring more users or taking even more free time from people. With rising competition in the digital media space, assuming a zero-sum game, the obvious answer is Meta will lose market share. But it is important to differentiate between its attention market share and its advertising market share. Although there is a ceiling to human attention, there is still growth left in the advertising space.

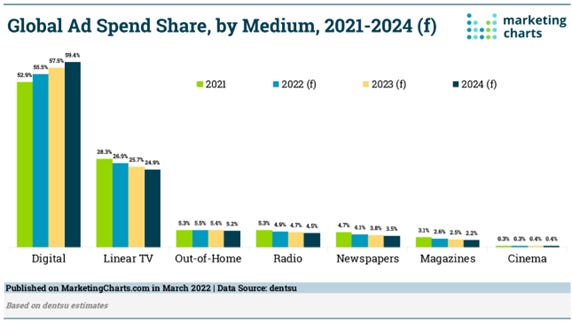

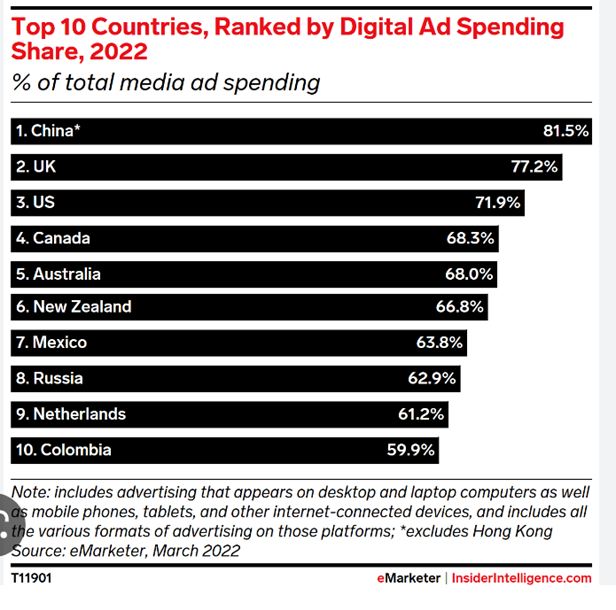

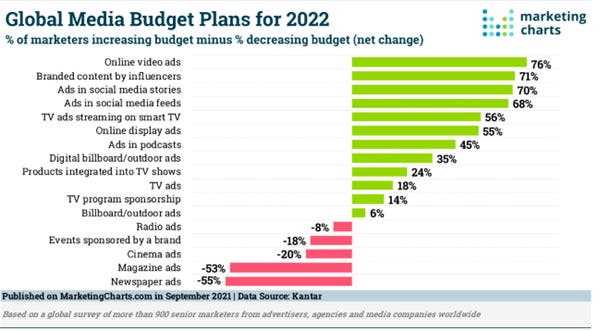

Since inception of the digital media, advertising has rapidly shifted here. In 2021, 65% of the global ad spend is digital. However, there is a large variance between geographic regions, where for example Latin America spends on 25% and China spends 70%. https://www.project-disco.org/competition/050420-evolution-of-ad-spend-and-the-dynamics-of-digital/

Also, surprisingly, some traditional media formats, such linear TV in 2021, still get 28% of the global ad spend. Furthermore, with traditional businesses such as large print media and media content owners, embracing digitization, ad spend to these areas may not go to zero either but forecasted at least in the near term to continue to decline.

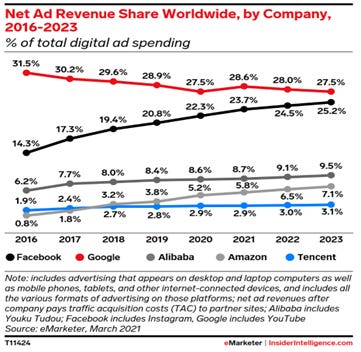

In the current state, Google and Meta, dominate the flow of digital ad dollars. Together they attract 50% of the global market share. Now, at these sizes, these 2 companies will experience the advertising cycle to a greater degree, but their duopoly protects their relative competitive positioning.

It is my best guess is that the combination of the ubiquity and ease of use of mobile devices, the evergreen human desire for entertainment, connection and curiosity, technological know-how using data to allow personalization, will continue to act as long-term tailwinds for the digital advertising. I don’t think it would be out to left field to forecast that global digital ad spend could reach as high as 70-80% in 10 years.

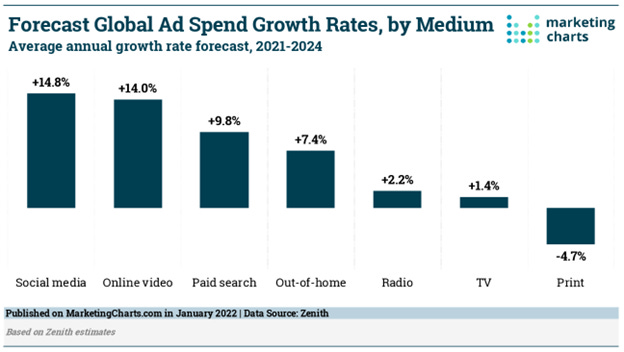

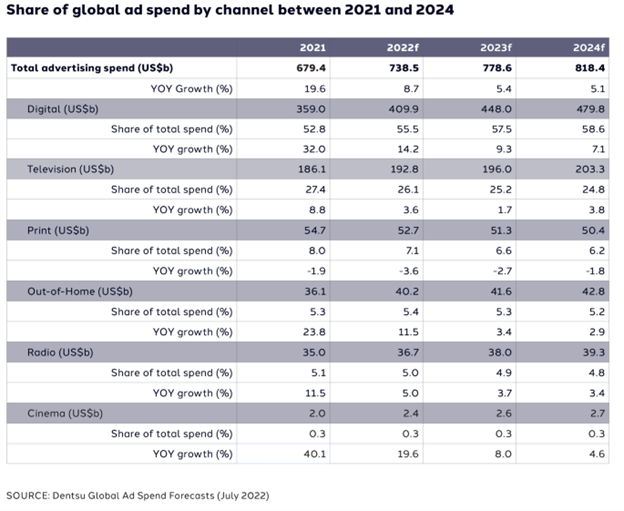

If worldwide GDP per capita (2021 - $12,263) grows at 4% (60-year average is 5.6%), with a population of 8.7 billion (2022 – 8 billion), and the following linear relationship between Ad spend per capita and GDP per capita holds up, the 2032 digital advertising market could be as larger as $653 Billion. I’ve included Dentsu’s 2024 forecast; my estimate seems to be in the ballpark.

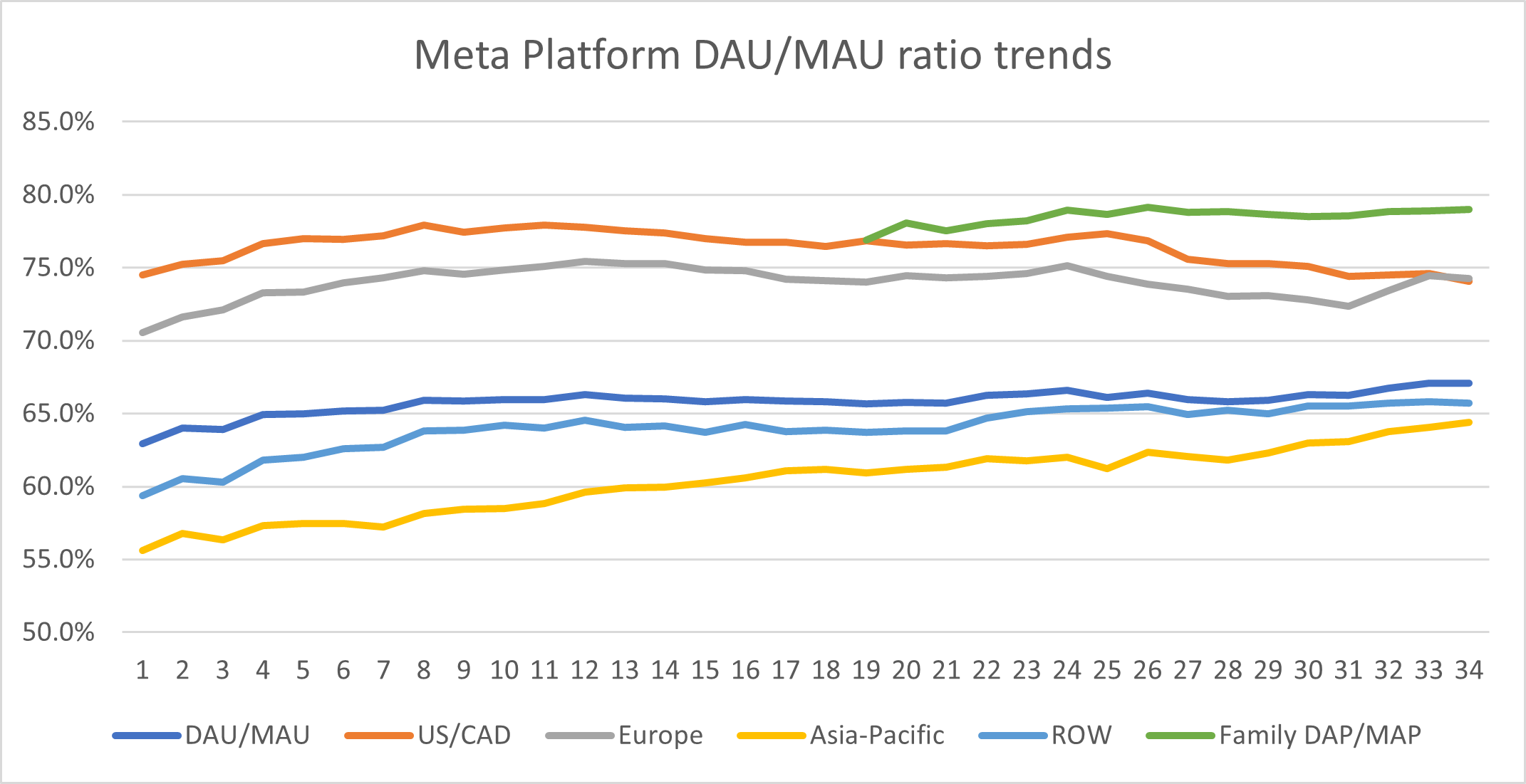

So even if the ratio of FoA users to world population stays consistent and their market share drops between 20-25% of total advertising spend, we are looking at a 2032 revenue of $130 to $163 Billion (2022e $114B). The key to getting here is user engagement. This can be loosely measured by following DAU/MAU and time spent per day trends.

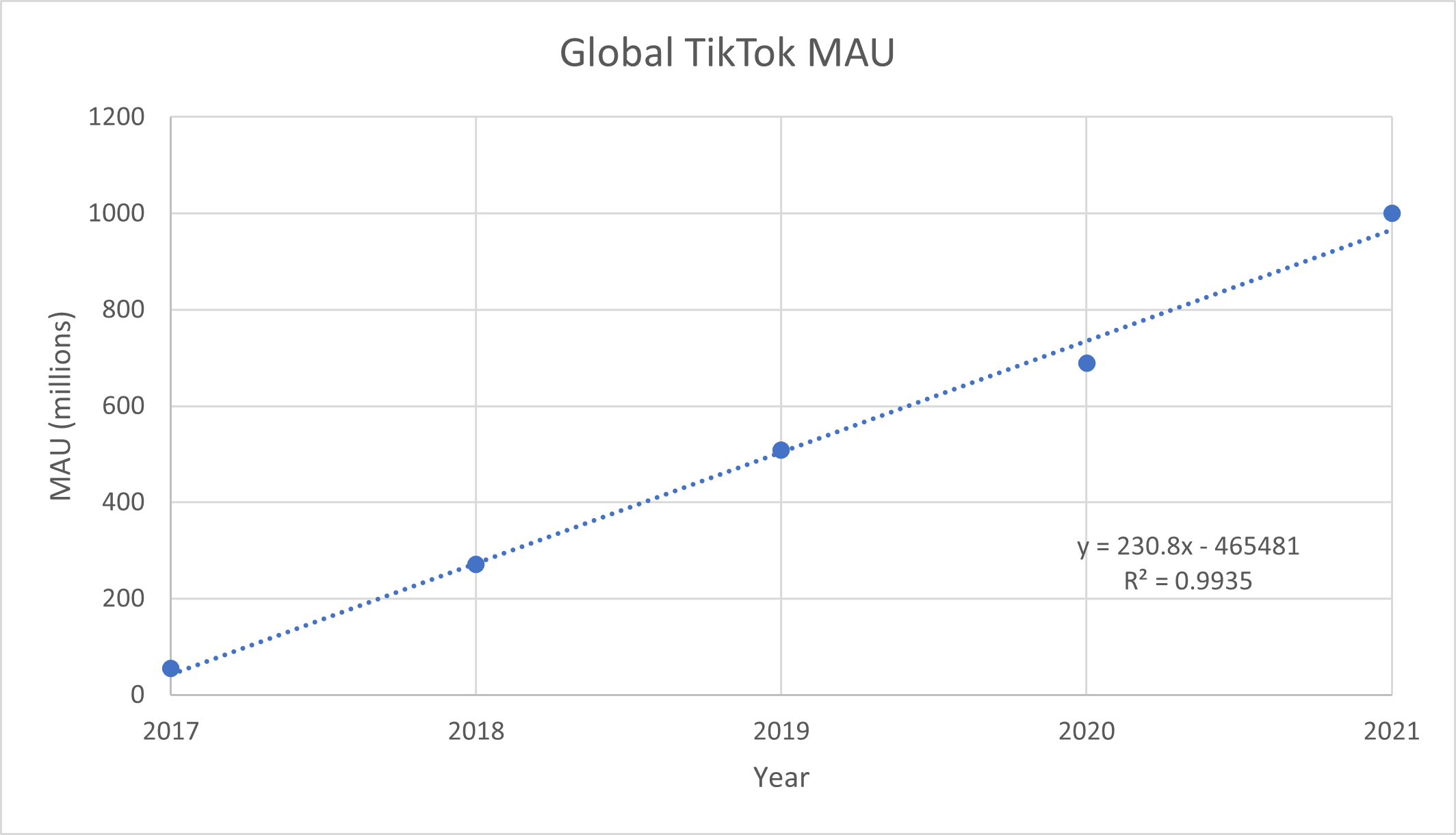

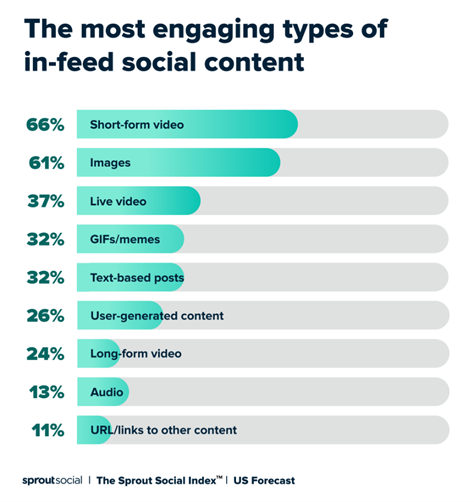

It takes a bit of faith to believe these numbers as it is highly dependent on their definitions and statistical processes to estimates these numbers. Contrast Meta’s numbers to the chart below among different social media platforms. Meta’s properties have performed well. There is some slippage in the US and Canada with respect to engagement since Q2 2020 which would coincide with the rapid rise of TikTok. Using free but incomplete data from Statista, my best guess is that TikTok has a global DAU/MAU ratio of 25-50%.

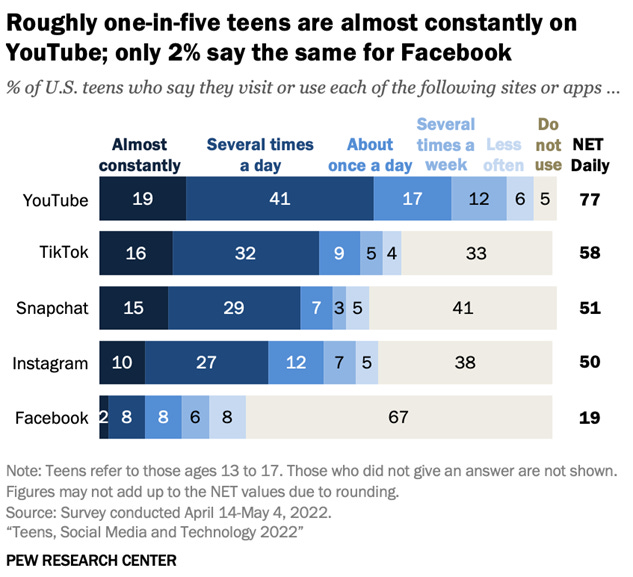

A 2021 Pew Research survey on US teen use of social media found that ~ 60% use TikTok daily which is 2nd only to YouTube. Snapchat and Instagram follow behind at ~50. Facebook has fallen from 70% to 30% in this 7–8-year time frame. With just under 50% of their advertising revenues coming from the US, protecting this market from competitors is important for Meta. In the US, TikTok clearly has won the teen mindshare from Facebook. Fortunately, Instagram is still in contention among this age group and demographically older cohorts are still quite wed to Facebook and Instagram. I can’t confirm if this is similar outside North America.

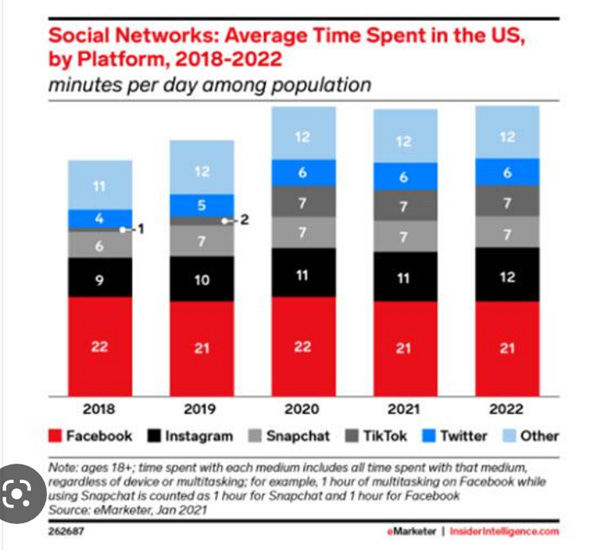

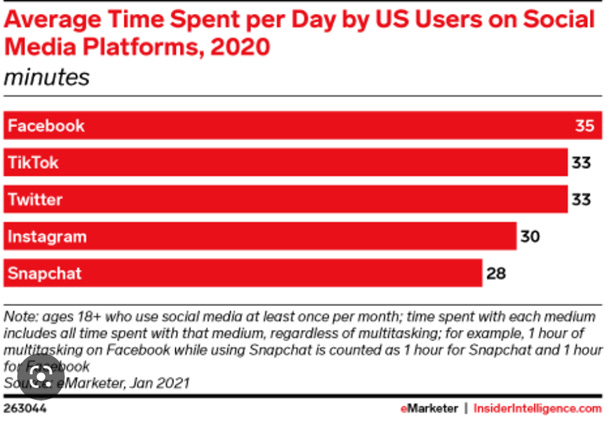

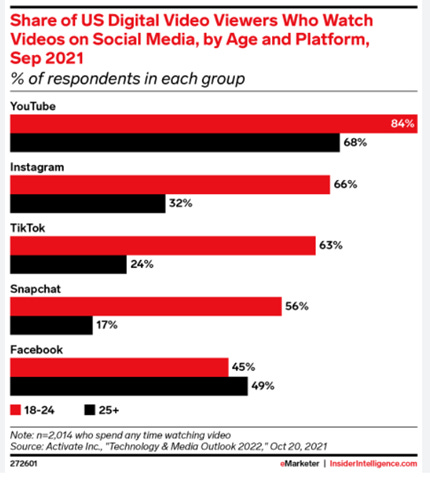

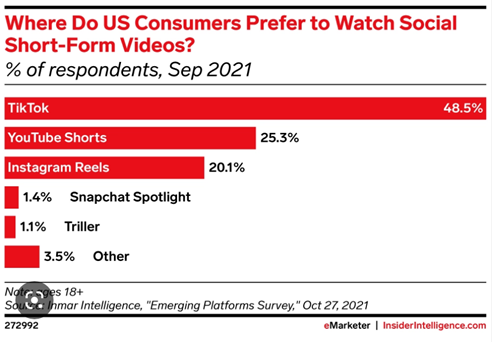

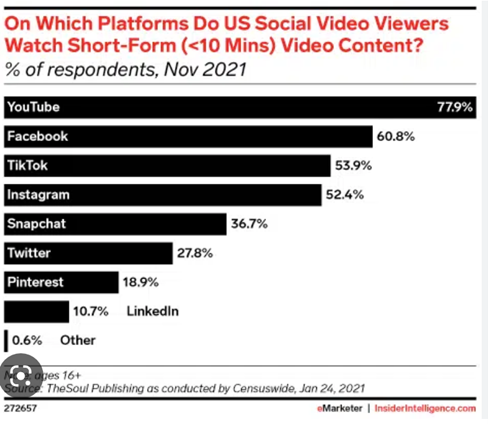

A16Z, a venture capital firm, had a post in 2020 that has several useful statistics on attention platforms. The Stickiest, Most Addictive, Most Engaging, and Fastest-Growing Social Apps—and How to Measure Them (a16z.com). Below are 3 graphics to consider. Unfortunately, there is no specific data on the FB Blue app or Instagram or TikTok. The data here is also a bit old as more recent 2022 statistics show that US users spend 45.8 minutes per day on TikTok, 45.6 minutes on YouTube, 34.8 minutes on Twitter, 30.4 minutes on Snapchat, and 30.1 minutes on Facebook and Instagram. (https://www.oberlo.ca/blog/tiktok-statistics). As a comparison, Facebook at its peak in 2016-2018, users spent ~ 45 minutes per day on it.

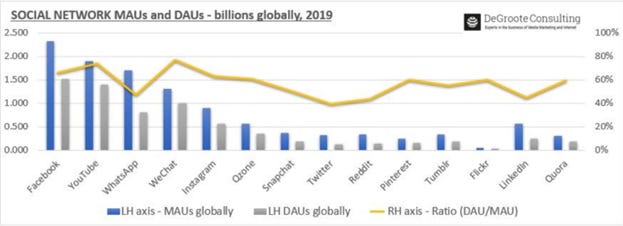

There is a plethora of charts and tables that one can find on Google search (I’ve included a several charts below). There is conflicting data which is difficult for me to resolve without having paid access. With such variability, I can’t conclude with anything with a high degree of confidence. But if push came to shove, I believe the FB Blue App, despite having a very large number of people, they have lost ground within the teen and early 20-year-old category especially in the US, both in terms of daily user numbers and time spent in-app. The only bright spot is that Instagram seems to be holding steady. My guess is that this is related to the explosion of “attention” competitors (paid streaming media (Netflix) vs social networks vs intent-based search engines (Amazon)) as well as people gravitating towards video content (definition: short-form (< 5 minutes – TikTok, Reels, YouTube Shorts) (long-form > 20 minutes – YouTube). MZ, in his Q2 2022 conference call, acknowledges that people are searching for the best content (especially video) and sharing those within smaller groups using dedicated messaging apps instead of directly engaging on Facebook or Instagram. He confesses that he was slow to identify this trend and is now pivoting to provide more AI-curated video content (Facebook and Instagram Reels) on their legacy properties. In the Q3 2022 call, MZ said the following with respect to their progress:

Our AI discovery engine is playing an increasingly important role across our products, especially as advances enable us to recommend more interesting content from across our networks and feeds that used to be primarily driven just by the people and accounts you follow. So this, of course, includes Reels, which continues to grow quickly across our apps, both in production and consumption. There are now more than 140 billion Reels plays across Facebook and Instagram each day. That's a 50% increase from 6 months ago. Reels is incremental to time spent on our apps. The trends look good here, and we believe that we're gaining time spent share on competitors like TikTok.

Over time, I expect a few things to set our products apart here. First is that our discovery engine work allows us to recommend all types of content beyond Reels as well, including photos, text, links, communities, short- and long-form videos and more. Second is that we can mix this content along posts -- alongside posts from your family and friends, which can't be generated by AI alone. And third is more social interactions move to messaging. We're developing a flywheel between discovery and messaging that are going to make these apps stronger. On Instagram alone, people already reshare Reels 1 billion times a day through DMs.

Undoubtedly, operating a social network media platform is not easy and keeping it relevant is even harder. The challenges can be summed up in 3 categories: 1) being relevant across generations and geographics, 2) maintaining stakeholder trust to continue to have a social license to operate, and 3) providing value to businesses that advertise and transact on top of their platform.

Tiktok and its AI-assisted content delivery short-video hacked the problem of rapidly scaling up user growth. This hack coupled with its talented co-founder-led team with $42 billion of cash on their balance sheet, operating profitability in Q1 2022, and having willing capital backers such as Softbank (Apple is an investor in their Vision Fund 1 that invested capital into Bytedance), has made TikTok a formidable opponent. With finite attention spans and advertising budgets, Tiktok is Meta’s greatest challenger.

MZ recognizes that AI-curated video discovery is key to maintaining relevance in this next-gen competition. Their $60-70 billion of capital expenditure this year and next is all dedicated to their FoA segments and reflect the high cost to transition and urgency to do so. If Reels can replicate similar success as TikTok and integrate their treasure trove of user data, Meta may just be able to stay in the game. It took TikTok 5 years to get to 1 billion users. Reels was introduced in 2019. It is fair to say that Meta needs to demonstrate substantive results by 2024 as it relates to Reels’ impact on time spent on their properties. Unfortunately for Meta, I think the base case will be that TikTok and Meta will need to share this attention market even if Reels proves to be successful.

As Facebook learned from scaling such a massive communication platform, extreme groups, hate speech, discrimination and bullying, and inappropriate behaviors will naturally spring up. With this known risk top of mind for regulators, TikTok will undoubtedly be challenged with the same problem amplified by the tensions between China and US. If such a division was to occur, I can only speculate that the attention and advertising market will be divided along similar lines. Faced with these issues, will Bytedance follow Meta’s lead and develop a multilateral oversight board to moderate content? Will both companies voluntarily limit the virality of potentially harmful content to reduce reputational risk at the cost of losing user engagement to the other? Which business will execute better to enable e-commerce on their properties and scale it globally? These are tough questions, and I don’t have any confident answers to them. But what I do know is the outcome will be dependent on MZ’s leadership relative to Bytedance’s. They will need to be laser-focused on motivate their employees to be maximally productive at the same time maintain cost discipline and be more opportunistic with their excess cash on stock buybacks to help keep their stock price as a useful currency. They need to move fast and not break themselves apart.

Although there are significant challenges, the saving grace is that their 10 million advertisers are not fleeing Meta’s media properties, yet. This gives them a bit of leeway. However, if their engagement drops or they fail to encourage more e-commerce within its walled garden, marketers, advertisers, and businesses will flow to where the demand is. It is surprising to me that they have not progressed further with their Instagram Shops, Facebook Marketplace (2016), Facebook Shops (2020), WhatsApp for business and WhatsApp payment rails more aggressively. Their “Payments and Other Fee Revenues excluding Reality Labs” seem stuck between $800 million to $1 billion annually. That said, Facebook Marketplace has 1 billion monthly visitors, Facebook Shops has 1 million monthly active Shops and 250 million monthly visitors.

What is the bottom line? There will be more digital ad dollars to capture in the future. Meta will have to share the attention market space with TikTok. MZ is motivated to keep Meta relevant which may include continued investments for the future and better financial decision-making particularly around stock buybacks. I think the most likely outcome is Meta will continue to be reasonably profitably and the terminal value at 10 years will not be zero.

So, what would Barry pay to own Meta?

I think the best way to look at this question is breaking up Meta into 3 components:

a) How much would you pay for its existing FoA business?

b) How much do you think WhatsApp and Messenger will be worth?

c) Deduct the expected value of its Metaverse spend (5% of a 10x, 95% of a zero).

The value of the existing FoA (excluding their messaging apps)

I drew various valuation ideas from Michael Mauboussian, Aswath Damodaran, and Geoff Gannon to construct a primitive DCF to give a ballpark range of intrinsic values. Here are the various key inputs:

- To estimate Meta’s revenues in the future, assumptions were made as it pertains to global GDP per capita, expected future population, linear relationship between Ad spend per capital and GDP per capita, Digital ad spend as a % of total advertising spend (2032 – 75%), and Meta’s market share of digital ad revenues (2032 – 20-25%).

- Using Mauboussian’s technique of capitalization of 100% of R&D, 70% of Sales & Marketing, and 20% of General & Administrative expenses over 6, 2 and 2 years respectively to derive a historical adjusted pre-tax operating margin of 50% and pre-tax ROC of 35%. I penalized their operating margins by 5% due to Apple’s App store policies and another 5% assuming higher inflationary pressures on employee wages. This gives me a current 45% and future 40% adjusted operating margin.

- Tax rate assumed to be 21%.

- Meta doesn’t really have much working capital investments required to grow; however historical capital expenditures have roughly been ~ 15% of revenues. Snap’s cost of goods sold is primarily related to their use of 3rd party cloud services to run its platforms. In 2021, they spent $1.75 billion for 530 million users, or $3.30 per user. This would translate roughly to $11-13 billion (10% of revenues) for Meta to run its FoA on 3rd party providers assuming 3.7 – 4 billion MAUs currently and in the future.

- This gives a 10-year run rate of $10-11 per share of Free Cash Flow assuming that all stock compensation expense is treated as cash expenses.

- Using a 3% terminal value growth rate to estimate a terminal value multiple and a 10% discount rate for my DCF, Meta’s FoA enterprise value is ~ $122 - $142 per share.

- Applying a 2/3 margin of safety, $81 – 95/share is a good entry point.

The value of WhatsApp and Messenger in the conversational commerce

According to Meta’s Q3 2022 earnings call, their messaging businesses are generating $9 billion in revenue. Messenger makes $7.5 billion, and WhatsApp makes $1.5 billion on 1.3 and 2 billions users respectively. Although conversational e-commerce is not popular here in North America, in Asia, it is significant.

I currently do not have a great source of information, but Statista estimates that this form of commerce generated $41 billion of revenues in 2021 and is projected to grow to $290 billion by 2025. Meta and 3rd party marketing materials suggest that when traditional e-commerce is combined with this form of communication, it is possible to achieve higher conversion rates. With such a large penetration of these 2 message apps, there is a potential for significant future growth. Meta recently disclosed that Click-to-WhatsApp grew 80% YOY.

Meta bought WhatsApp in 2014 for $21.8 billion when it had 450 million users or $48 per user. At 2 billion users today, this would be worth $96 billion or ~$35/share. Although there is no publicly available messaging app to compare to, we can make a subjective WTP (willingness to pay) judgment as to WhatsApp/Messenger’s utility relative to various consumer-based subscription services.

Spotify – $120 per year

YouTube Premium - $144 per year

Netflix - $120 - $240 per year

Apple One individual plan - $180 - 360 per year

US Amazon Prime - $139 per year

AT-T Value and Unlimited Premium plans (1 line) - $500 – 1000 per year

Canadian Internet services - $360 – 2000 (CAD) per year

It would be believable that a WhatsApp/Messenger user might derive at least $10 – 50 of utility per year. With 3.3 billion users, this would have an annual revenue run rate of $33 - $165 billion. Assuming that operating margins could be between 30 – 50%, the total value of this enterprise could be between $99 - $825 billion or $37 - $305/share. The following shows some popular messaging apps in 2022 and their monthly revenues. Many have offered services on top of their free messaging capabilities.

With its current revenue at $9 billion, 3.3 billion users, an assumed 30-50% pre-tax operating margin, at no growth, WhatsApp/Messenger is worth $27 – 45 billion or $10 – 17/share. This is most possibly way too conservative, but it is an anchor point. If I assume that WhatsApp can achieve the same revenue per user as Messenger ($5.76/user), then WhatsApp could be worth $35 – 58 billion or ~ $13 – 21/share by itself (remember the original purchase price was $21 billion). Together with Messenger ($22 – 38 billion or $8 – 14/share), they could be valued at $21 – 35/share. Another more aggressive way to look at this, particularly with a growth outlook is valuing them at an upper limit of 10 x sales, which translates to $90 billion or $33/share. As a related comparison, Snap is valued at $33/user (Nov 16, 2022), so at 3.3 billion users, WhatsApp/Messenger could be worth about $109 billion or $40/share. If I had to hone down on a conservative estimate, it would be between $21 – 33/share. Applying a 2/3 margin of safety, a good entry point would be $14 – 22/share.

Putting it together

Using 2.7 billion shares outstanding and the following estimates:

FoA = $122 to 142/share

WhatsApp/Messenger = $21 to 33/share

Metaverse bet = - $32 to -19/share

Cash = $15/share

Debt = - $10/share

Given that the cash on hand will not be returned to shareholders via dividends, and if stock buyback continue to only prevent stock dilution from options issuance regardless of market prices, to be conservative I should ignore the cash. That said, the cash on hand will most likely be used on the metaverse bet, so netting it out against the Reality Lab spend, would be logical.

So, my intrinsic value assessment is between $116 - $161/share. Incorporating a 2/3 margin of safety, the range to buy Meta Platforms would be between $77 - $107/share.

In a prior post, I mentioned that I would be a purchaser of Meta at $100/share. To be transparent, I had a buy limit order which I took off just before the disastrous earnings call. Although I had done some work on it, I felt compelled to write down my thoughts before committing to any final action to bring my holding to a 5% position. After writing all this out, I feel that I have reached a better point to decide with my eyes wide open.