Missing out on Shopify

Missing out on Shopify

or will there be a future reasonable entry point?

In 2018, a non-finance day-trading friend suggested to me that Shopify is a great stock to own especially since it just IPO’ed and it had a great story. It was currently undergoing a short attack by Citron Research. It was a high tech flier with big multiples and had negative earnings per share. At that time, I was convinced the only way to invest was to do it the “value” investing way and rapidly dismissed his proposition without thinking much about it.

In 2019, after disproving the Citron Research short thesis, Shopify’s price climbed rapidly in the $250-$300/share CAD range. I focused on its sales and tried to construct a base rate sales growth model using Michael Mauboussian’s base rate book and create a simple discounted cash flow model. I said to myself, I won’t purchase this unless it gets to $200. Needless to say, it never returned to this price.

In 2020, I remember looking at Shopify in March with its price dropping down to $700/share CAD. I again missed this opportunity because I lacked cash, hadn’t done enough homework, and had a limited investment framework despite recognizing that Tobi Lutke was a stellar founder.

Three opportunities, three strikes. Now that the price expectations are so high, I have permanently missed my chance.

Or not……

If I could take anything from this experience, these would be the lessons:

1) Always keep an open mind,

2) Do your homework to be prepared,

3) Consider including quality businesses with long-runways in your wish-list despite price run-ups as the core product(s) have gained acceptance and the business has been de-risked.

There have been countless articles/podcasts from stellar analysts that will undoubtedly be better written and provide much more useful insight into Shopify. The following are some of my favourite and a few key takeaways:

Yet Another Value Podcast - with Minion Capital (Shomik Ghosh) on Shopify and VC investing [October 2, 2020]

Software is easily replicated by others, so asset-light business building asset-heavy components (without leverage) can help solidify head-starts (moats) from them competition - Netflix, Amazon’s AWS, Zillow, Spotify, Shopify are examples of this behaviour

Capital allocators in high valuation businesses need to consider expanding their TAM by moving into adjacencies with their excess free cash flow or raising public market capital at opportunistic times to capitalize on these chances - Shopify has made a series of public share offerings at fair value to overvalued prices

When a large incumbent moves into the opportunity space, this is validation of its worth - Amazon moving into Shopify’s business model

Targeting end-user vs CIO/CTO/CSO dictates low cost entry, viral marketing, greater churn vs higher subscription prices with longer term contracts with a formal sales force - Shopify’s offerings straddle both

The relative valuation is high but Shopify accounts for 7% of US e-commerce and there are lots of international opportunities ahead, therefore its absolute valuation may still be reasonable

Competitors such Square (POS), BigCommerce, Wix (website development), Mailchimp (CRM) are all attacking Shopify at various points of entry

Shopify’s talent funnel and retention is really good

What We Learned from Our Biggest Mistake in 2017 | MOI Global with Michael Shearn

Partner with Mt.Rushmore founders in businesses that can self-fund, have strong balance sheet, a growing total addressable market or ability to move into product adjacencies, and passionately solving customers’ problems

Shopify: Going Direct To Unlock Ecommerce | Seeking Alpha with Benedict Evans

Building tools to allow retailers to unlock e-commerce independent of Amazon - Amazon can’t swallow everything e-commerce, just like Walmart can’t swallow everything physical

Building a Modern Business - Invest like the Best with Tobi Lutke

Tobi Lutke’s differentiated view on how Shopify competes and his ideas on how to build his company

“Focus of audience ends up being, amongst all the things that you could have focused on, one of the most significant predictors of the success of a company because it's very, very easy to get diffused between different stakeholders that you're building something for” - the importance of customer focus

“Shop is not a marketplace in the traditional sense. It's actually more like a shop of shops. You're discovering merchants and brands to follow. And the products you see are based, partly algorithmically, but based on the people you have already purchased from. Shop is much more about intensifying the relationship that buyers have with the brands they've purchased from, rather than doing kind of the opposite, which is what most marketplaces do.

Most marketplaces actually point you to a larger variety because a marketplace derives its power from the opposite of being friendly for the merchants. In fact, in most marketplaces, the merchants' margins are the opportunity and the future fees of the marketplace in every category. And so the marketplace actually derives power by diffusing the influence of any individual merchant. And so it pits people against each other and those are challenges that are very, very difficult to handle” - Deferring immediate and obvious monetization opportunities for their customer’s successes

"You know what? Instead of trying to get people to change their mind, let's just make it simpler for them to do the thing that we want them to do." - on building culture at Shopify

“we're trying to create a process-light company, where basically we say, "Hey, we trust each other. We even have language around trust in the company or under trust boundaries and use your best judgment. And let's collaboratively inquire into this problem that we want to solve” - on how to avoid bureaucracy

“you had a finite amount of information at a certain point. And of course you need to make a decision, too. You can spend forever creating context. You have to kind of make a decision somewhere between exploring 40% and 70% of the entire problem space, because otherwise it just takes too long” - on making decisions

Platforms, Ecosystems, and Aggregators - Invest like the Best with Ben Thompson

Shopify is trying to become a platform with merchants on top and the e-commerce supply chain at the bottom (such as 3rd party logistics) - Shopify is more analogous to Microsoft and AWS than 3rd party marketplace aggregator

Merchant churn is not particularly relevant given the low to zero marginal cost of failure with their software-as-a-service products

Shopify does not compete with Amazon directly with a marketplace and doing so would be extremely difficult

Analyzing Bitcoin’s Network Effect with Lyn Alden

This article was particularly helpful in summarizing the math for different networks. One-sided networks (telephones, Facebook) follows Metcalfe’s law where “connections (c)” = 0.5*”nodes (n)”^2 as the network grows extremely large (if small c = 0.5*n*(n-1)). Two-sided networks (payment systems, Ebay, Amazon’s Marketplace) follow “c” = “sellers” x “buyers”. Two other great insights, in terms of successful networks, is the ability for their network to be 10x better than the next and for it to reach $100 billion in today’s valuation.

Fundamentals Demystified: Shopify, Valued 1.7x Higher Than Their Total Addressable Market (NYSE:SHOP) | Seeking Alpha with the Oracle of Alpha

“Whoa! No denying that $4.2 trillion is one big number. Don't get too excited just yet though, remember that we've previously established Shopify generated roughly 1.55% of GMV in revenue. While still an incredibly large number, it drops all the way down to $65.20 billion. This is of course a phenomenal improvement over FY19 merchant solutions revenue of $935.9 million, but it's still only 55.2% of their current market cap and still requires a 100% monopoly on all retail e-commerce sales, which is obviously not even a remote possibility.

Shopify included internal TAM estimates in their 19Q3 investor deck, but it unfortunately does not separate between subscription solutions and merchant solutions and only gives a specific number for SMB's -- $70 billion.” - Shopify’s March 2021 Market cap is $140 billion

Shopify: A Good Buy For Consumers, Not Investors | Seeking Alpha with Satya Damaraju

Using 5 and 10 year analysts consensus estimates, 10% WACC, the valuation should be $376 and $931/share USD.

Shopify: Every Growth Picker's Dream Beset By Heady Valuations

Excellent summary of Shopify’s current value drivers

How to value Shopify with DCF? Is it overvalued? by Wealth Workout

A deep dive into the constructing a DCF

Shopify: The best operating system for commerce by Eric Sprague

Discusses the competitive dynamic between Shopify, Big Commerce, Demandware, and Magento.

All these financial write-ups agree that Shopify is great business but the biggest risk to this investment is its persistently ebullient valuation. The same thing has been said about Amazon over the years. Below is an illustration of all the opportunities to buy Amazon at ever increasing prices and still get a decent return.

My non-expert approach to valuation

There are 3 edges that any investor can have: informational, analytical, and behavioral. In my position as an outside passive minority investor with only public information and limitations to forecast sales, margins, and other important financial estimates, trying to construct a discounted cash flow model is a losing proposition.

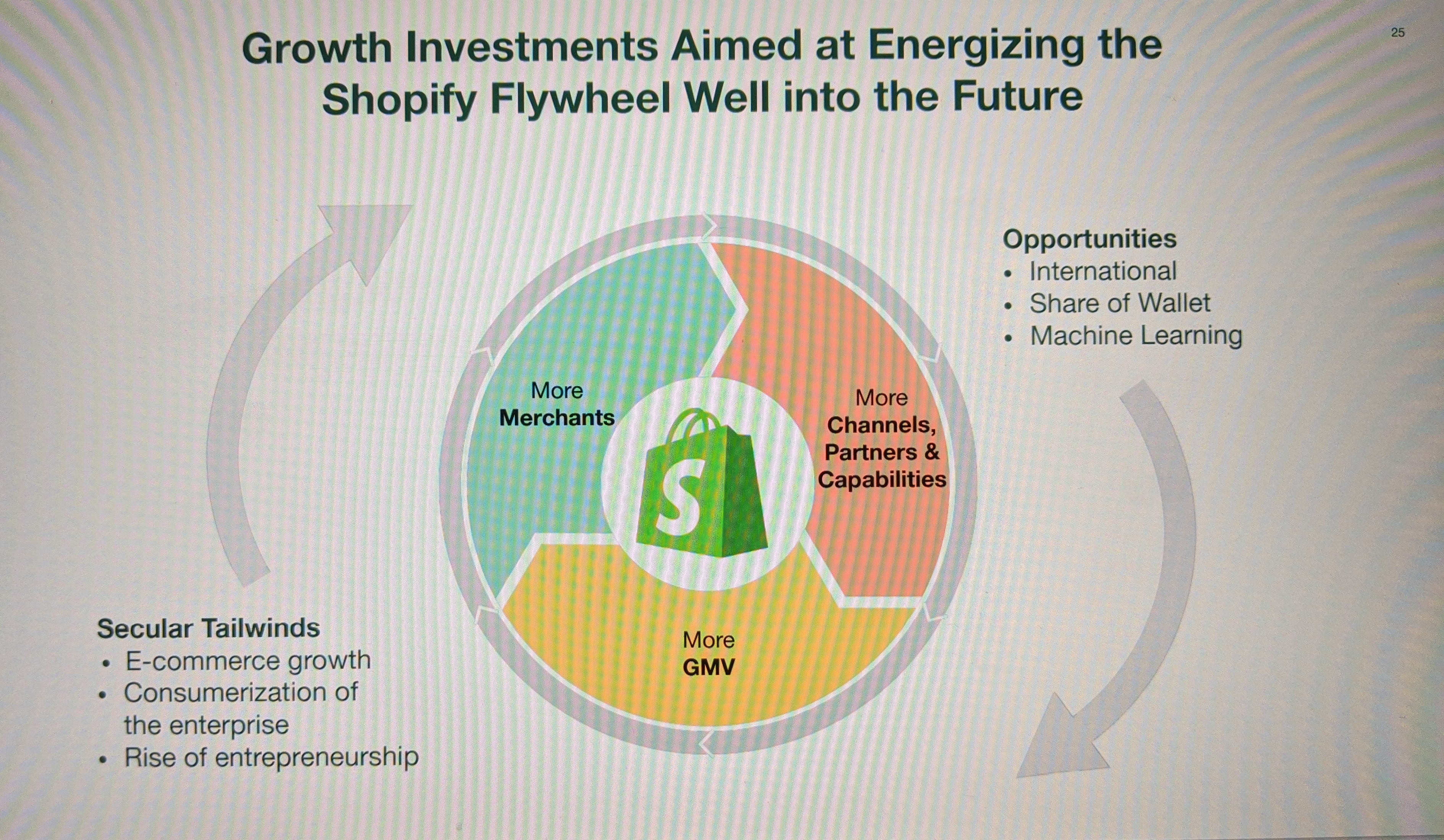

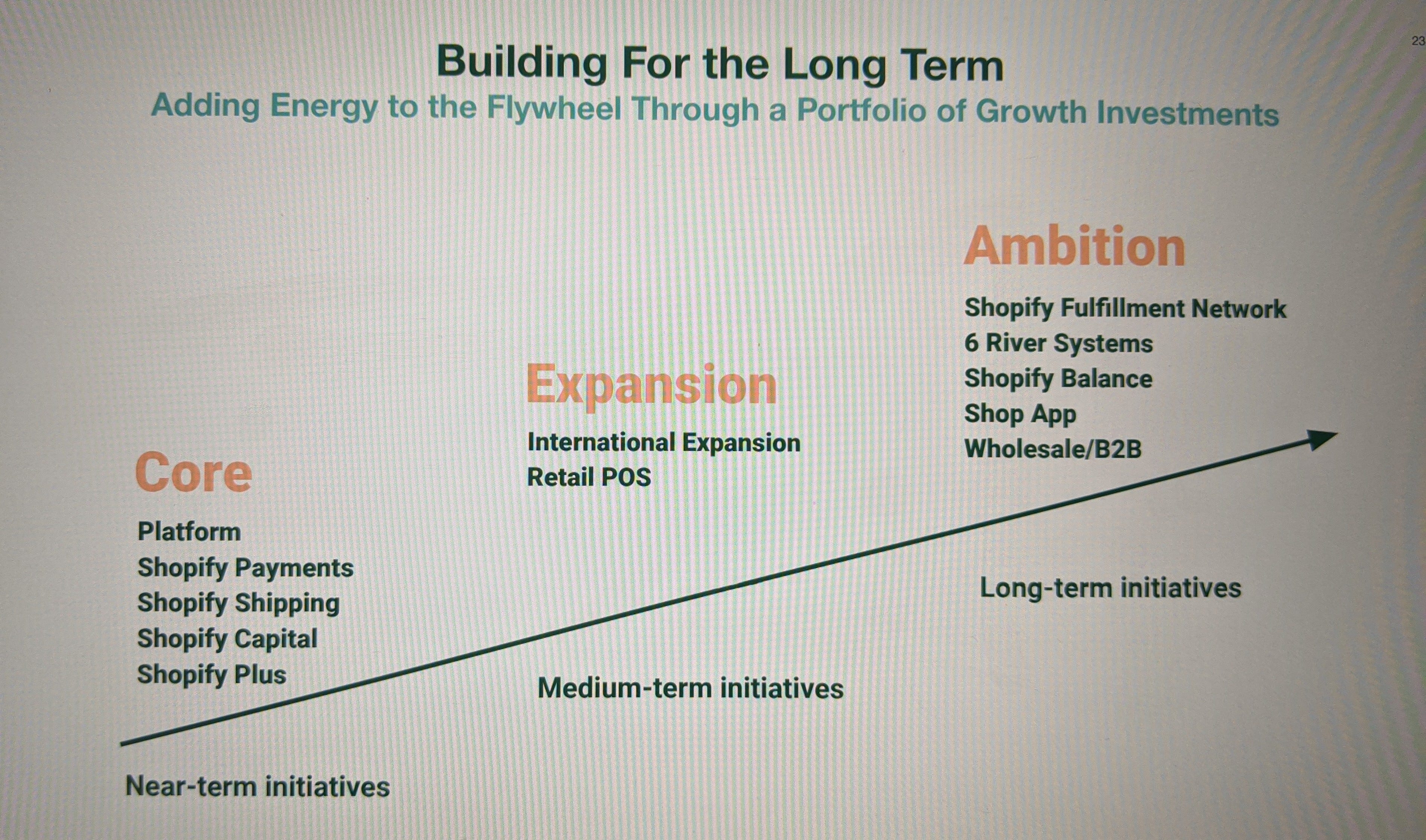

However, I still need to derive some numerical range to make sure that I’m paying for a reasonable price to get an acceptable return. I think it helps to conceptualize the Shopify operating system flywheel. Below is useful chart found in their investor’s presentation:

Central to their business model are the number of merchants, the number of partners, and the amount of Gross Merchandise Volume (GMV) generated. There are a couple of ways to model this out.

Model #1 (the really simple but probably wrong one)

My children get extra math help via an after-school program called Spirit of Math. They have this question: If there are 10 people a room and they all shake hands with each other, how many hands shakes will there be? The answer being 10 x (10-1) / 2 = 45. This is Metcalfe’s law. The value of the network is the number of connections that it has. This can be used to value Facebook, Bitcoin or any one-sided network.

Shopify (like Microsoft) is more like a two-sided network. Merchants on one side and Partners on the other. The number of connections is equal to the number of merchants x the number of partners. I know this is gross simplification and that a small number of merchants and partners account for the majority of the value. Unfortunately, Shopify doesn’t break this out.

In 2015, there were 1.03 billion possible connections with it steadily growing ~100% per year. At the end of 2020, there were 36.9 billion possible connections.

The value of these connections is the sum of all the incremental merchant revenue gains and partner cost-savings that arise from using the Shopify’s OS and their willingness to stay vs their alternative. There is no easily obtainable source to determine the precise dollar value and all their estimated retention rates.

However, if I assume that over time, the stock market is efficient and in aggregate will be correct in guessing the “value of the Shopify network” as reflected by its stock price. It’s long-term price trend should reflect all the discounted expected cash flows and its profit levers. I probably won’t be smarter in triangulating these flows.

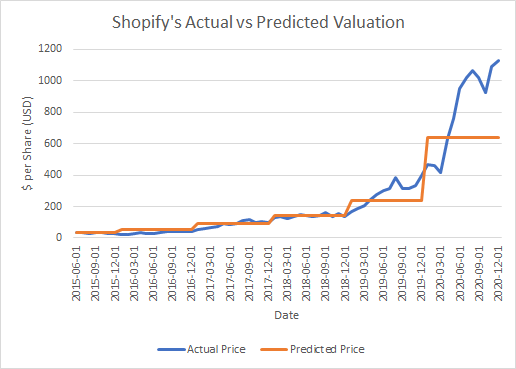

Ideally, we have a very long-term price history on Shopify, but published data only goes back to 2015. However, 6 years of data is better than 1. So using this data, I tabulated the enterprise value per connection for each the years, deriving a value of $2.11 per connection with a standard deviation of 0.51 and coefficient of variance of 0.24 (<0.3 is really good). The median was $2.08 with 25th and 75th inter-quartile range of $1.85 to $2.43. Fortunately, these summary statistics are quite tight.

Below is the price chart with the estimated Enterprise value per share since its 2015 IPO.

It is apparent that the current market value is much higher than its predicted value. So it would seem obvious that Shopify is too pricey to warrant attention. However, there are a few considerations:

1) The Covid-19 pandemic validated the need for Shopify’s existence. When the physical retail economy was shut down, the need for an online presence is vital to survival and that incumbents like Amazon and upstarts like Wayfair, Etsy, etc won’t eliminate Shopify’s value proposition.

2) Shopify has consistently innovated and introduced new product features over time to grow it’s GMV share.

3) Global retail sales is ~ $24 trillion in 2020 and growing 5% per year. E-commerce is a growing secular trend. The current total addressable market ~ $4.2 trillion and projected to grow to $6.5 trillion by 2023. With e-commerce accounting for 15-20% of global retail sales, I would expect this penetration should continue upward (ie 50%? in 10-20 years).

4) According to their 2020 Q4 investor presentation, AMI partners estimates there are 68 million retail business globally. They currently have 1.75 million merchants on their platform. They have been consistently growing merchant numbers annually by 45-55% since their IPO. Again, lots more room to grow.

5) The Shopify partner ecosystem is also been consistently growing annually by 30-35% since their IPO. They share their subscription revenues with their partners and help them create an annuity-like revenue stream as long as their product and services are used by the merchants. Everyone is aligned to succeed and drive GMV through the Shopify platform.

6) Shopify’s model is a hybrid between Microsoft and Costco. This differentiates it from marketplaces like Amazon, Wayfair or Etsy. Merchants are not commoditized and dis-intermediated from their customers. Saavy merchants will recognize the importance owning their customer relationships. Tobi has reinforced that he has no plans to turn the buyer-facing Shop app into a marketplace which in my opinion is the smarter long-term strategy. This allows all stakeholders to ride the success flywheel together and attracts more future participants. It is thought that Shopify’s merchant churn rate decreased from 10% to 5.6% today. Similarly, it seems that app developers are increasingly attracted to the Shopify platform as discussed in digiday.

7) Shopify’s take rate is currently 2.6% inclusive of subscription fees and merchant solutions. In 2018, Alibaba, Amazon, eBay, and Mercardolibre had take rates of 3.3%, 13%, 8% and 7%. With accelerating product innovations, this take rate should also increase with time.

If these considerations imply that there is continued growth in merchants and partners, then the value of Shopify’s platform should still have growth ahead of it.

The # of merchants has been growing on average at 54% and 55% pre- and post-Covid with a coefficient of variance of 0.3. The lowest growth rate was 30% with the IQR25 at 45%. The growth in # of partners has been a bit more volatile but the median rate is ~36% and 33% pre- and post-covid. The lowest growth rate was 20% with the IQR25 was 29%. I projected its enterprise value per share few years into the future using the lowest and base historical rates which is illustrated below…

Using the enterprise value per share on March 15, 2021 of $1,083/share, the 3-year IRR could range between 25-56%. Assuming an average annual 9% stock dilution drag, the IRR would be between 16% to 47% in the next 3 years.

Model #2 (The slightly more complicated but more realistic model)

There are a few major problems with Model #1:

it is reliant on the market valuing the Shopify platform and on the short-term could be very wrong,

the relationship between enterprise value and # of connections remains stable over time,

the network connection calculation is very crude,

the market multiples will contract with slowing growth rates and increasing inflation expectations.

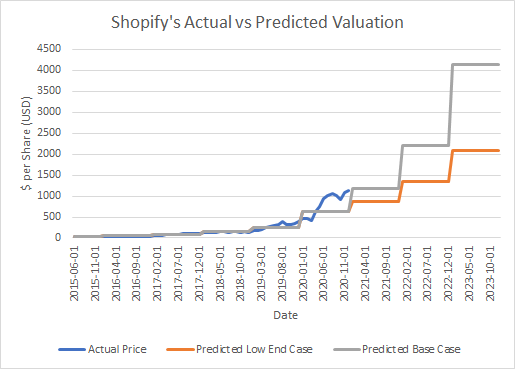

Model #2 seeks to predict GMV directly with more explicit assumptions.

Total merchant growth rate starts at 45% and declines 10% per year for 7 years (reaching ~20% of global merchant market share),

Plus merchant as a % of total merchants is stable at 0.6%,

Estimate total GMV relative to # of Plus merchants using $8.25 million per Plus merchant

Take rate (inclusive of sub fees and merchant solutions) start at 2.66% and increases 15% per year (take rate at year 7 equating to ~7%),

The EV to sales multiple contracts from a normalized current value of 60x to 10x. 10x was based off a future net margin of 25% and relative to an S&P return of 7.5% and long-term PE of 16.

CAD/USD fx rate of 1.17 (long-term average exchange rate)

Using a personal return rate of 13% plus 9% stock dilution, the required discount rate is 22%.

The average fair present value from this exercise is ~ $1,344/share CAD or $1,148/share USD. The share price (March 15, 2021) is $1,445/share CAD or $1,159/share USD. My best guess is that my fair value should range somewhere in between $1,060 to $1,760/share CAD or $906 to $1504/share USD.

So at least from these calculations, it would appear that Shopify is a great business trading at fair value. It’s no bargain, but doesn’t appear to be ridiculously over-valued.

Incumbent on following Buffett and Munger’s advice of buying great businesses at a fair price, will depend on management execution in terms of innovation and capital allocation with a good dose of secular tailwinds.

The following is a list of observations that give hints to these required elements (in not particular order of importance):

Founder participation and ownership skin-in-the-game,

Tobi has moved back into product development and delegated operational management to Harley,

Raised equity capital in the past at fair prices and most recently at over-valued prices,

Focusing on solving merchant and partner problems and not managing the take rates,

Very few acquisitions to minimize future technical debt to its software platform,

Incentive alignment by sharing 80% of fee streams with app development partners,

Incentive alignment by under-pricing their subscription fees and tying their success by GMV dollars,

Moving into capital intensive infrastructure development to solve related merchant logistical problems that would be hard for other capital-light business competitors to clone,

the network has been de-risked in terms of product acceptance and passed the Michael Saylor $100 billion market cap size threshold,

Growth rates far exceed their other competitors (eg Big Commerce) during the Covid-19 pandemic,

Secular e-commerce upward trends and growing realization of omni-channel compounding effects on merchant success.

Conclusion

This time around I’m better prepared. There are still knowledge gaps especially around execution risks and competitive dynamics. At this stage, I might be willing to bet up to a total of 2.5% of my portfolio on Shopify; value averaging in over the next year. The only thing certain is that amateur retail investing is really hard…